As climate reporting shifts from voluntary pledges to mandatory disclosure, companies are increasingly combining science-based targets, net zero management systems, and regulatory reporting frameworks to demonstrate both ambition and execution. Rather than operating as standalone initiatives, frameworks such as ISO 14060, SBTi, IFRS S2, and ESRS can be viewed as complementary components of an emerging three-layer Climate Accountability Stack, connecting implementation, credibility, and disclosure to help organizations move from climate commitments to measurable progress.

The net zero standards landscape is entering a new phase. For years, companies have struggled with a crowded mix of voluntary frameworks, investor expectations, carbon accounting rules, and climate disclosure requirements. Two of the most significant recent developments are the draft ISO Net Zero Aligned Organizations Standard (ISO 14060) and the Science Based Targets initiative’s Corporate Net-Zero Standard Version 2.0. [1][2]

Both aim to improve the credibility of corporate net zero claims. But they are not interchangeable. ISO 14060 is emerging as a broad, internationally harmonized standard for net zero transition planning and alignment, while SBTi remains a more prescriptive target-setting and validation framework focused on emissions reductions aligned with climate science. [3][4]

A Brief History of the ISO Net Zero Standard

ISO’s work on net zero began with the ISO Net Zero Guidelines, IWA 42:2022, launched at COP27. The guidelines were developed to create a common global reference point for what “good” net-zero action should look like across organizations, cities, regions, and countries. ISO describes IWA 42 as a framework intended to align territorial approaches, such as national or city net zero plans, with organizational and value chain approaches. [2]

The draft ISO 14060 standard builds on those 2022 guidelines. ISO released the draft for public consultation June 2026, describing it as the world’s first international standard for net zero alignment and a tool to support credible, comprehensive net-zero transition plans. [1] Public consultation ends in August 2026 and the final publication is expected in 2027.

The significance of ISO 14060 is that it moves net zero from guidance toward a more formal, potentially certifiable and independently verifiable management-system-based standard. That matters because ISO standards are already widely used by companies for environmental management, quality, safety, and risk systems. For companies that already use ISO 14001 or other ISO management systems, ISO 14060 may be easier to integrate into existing governance, controls, documentation, and assurance processes.

A Brief History of SBTi’s Corporate Net-Zero Standard

The Science-Based Targets initiative was launched before the Paris Agreement and has become one of the most influential voluntary frameworks for corporate emissions target setting. Its Corporate Net-Zero Standard gave companies a science-based pathway for setting near-term and long-term emissions reduction targets, with an emphasis on deep value chain decarbonization before neutralizing residual emissions.

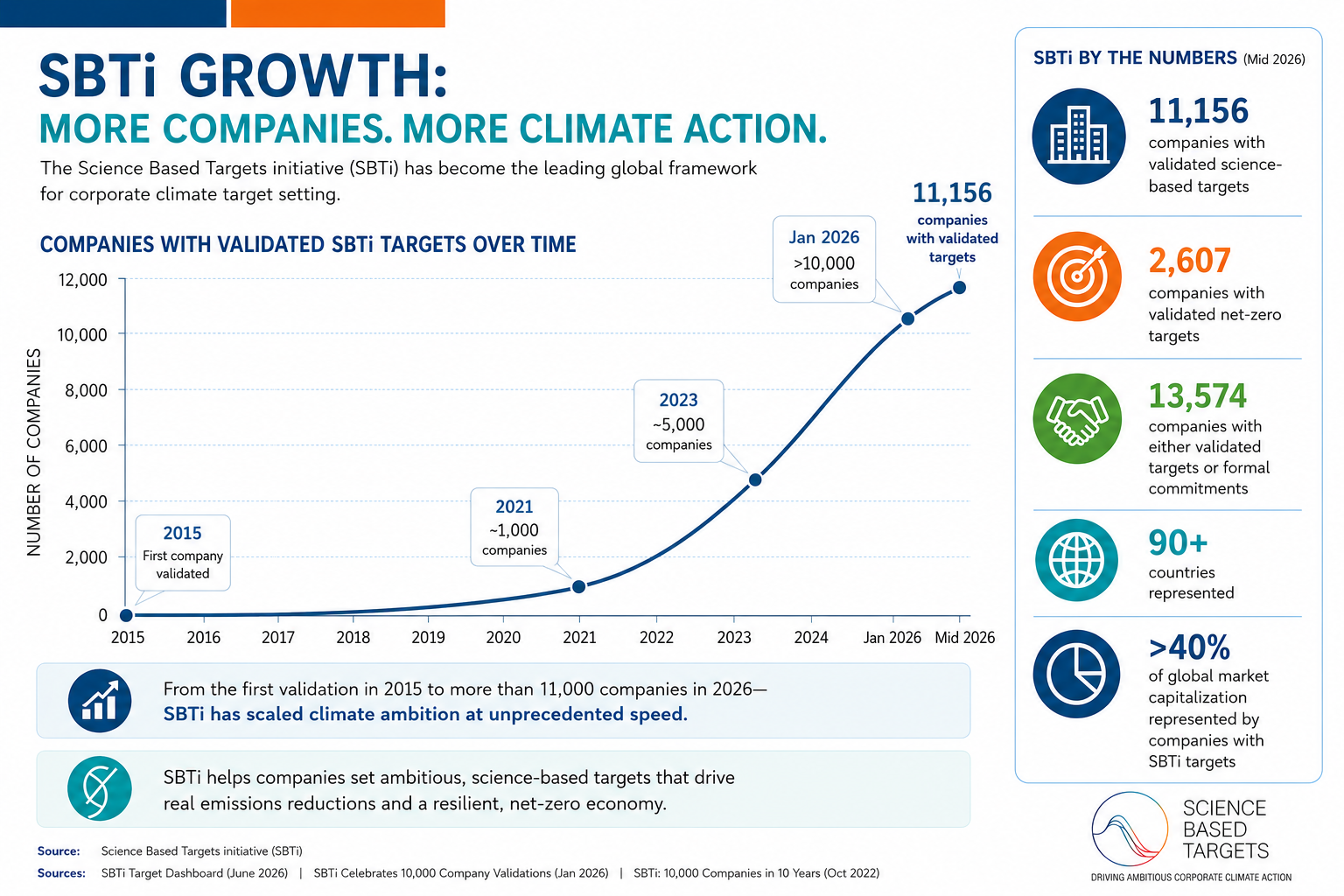

SBTi’s Corporate Net-Zero Standard Version 2.0 was developed through a multi-year revision process. According to SBTi, the Version 2.0 revision process included two public consultations and extensive pilot testing involving 1,800 stakeholders, with more than 320 companies participating in the first phase of pilot testing and more than 50 in the second. [4] Version 2.0 was released this month (June 2026) and is described by SBTi as its most comprehensive framework for corporate climate action to date. [3] Validation against the new standard is expected to open in early 2027.

Where ISO 14060 and SBTi’s Corporate Net-Zero Standard 2.0 are Similar

ISO 14060 and SBTi’s Corporate Net-Zero Standard 2.0 share several important principles. Both are designed to increase credibility in corporate net-zero claims by:

- Emphasizing the need for near-term action rather than distant 2050 commitments.

- Recognizing that organizations need accountability, implementation standardization, actionable emissions measurement, transparency, and progress reporting.

Both also respond to the same underlying problem:

- Corporate net zero claims have often been inconsistent, poorly defined, overly reliant on offsets, or disconnected from real operational decisions.

In that sense, both standards are part of a broader movement away from aspirational climate commitments and toward evidence-based transition planning.

Where ISO 14060 and SBTi’s Corporate Net-Zero Standard 2.0 Differ

The biggest difference is purpose. SBTi is primarily a target-setting and validation framework. It is best known for defining whether a company’s greenhouse gas reduction targets are aligned with climate science. It is especially relevant for companies that want externally validated emissions reduction targets that investors, customers, and disclosure users recognize.

ISO 14060 is broader. It is focused on net zero alignment and transition planning, not only target validation. It may be better understood as a management-system-oriented standard that helps organizations structure their net zero strategy, governance, implementation, and assurance approach.

Another major difference is audience. SBTi is designed primarily for companies. ISO’s net zero work is intended to be useful across organizations, policymakers, cities, regions, and other institutions. ISO’s 2022 guidelines explicitly aimed to align territorial and value chain approaches. [2]

There is also a difference in how each establishes credibility. SBTi validates targets. ISO standards, depending on the final structure and assurance ecosystem, may be used more like other ISO standards: as a basis for internal controls, third-party assessment, and integration with management systems.

When SBTi May Be the Better Fit

SBTi may be the better choice for a company seeking recognition by investors, customers, employees, and rating organizations. It is particularly useful for companies facing pressure from large customers, lenders, or sustainability ratings platforms to demonstrate that their Scope 1, 2, and 3 targets are aligned with climate science.

SBTi is also likely to remain the stronger option when the primary need is emissions target credibility. For companies with mature greenhouse gas inventories, strong Scope 3 data, and a desire to make public climate commitments, SBTi provides a structured pathway for setting and validating targets.

When ISO 14060 May Be the Better Fit

ISO 14060 may be more suitable for organizations that need a practical net-zero management framework rather than only a validated target. This may include companies that are earlier in their climate journey, organizations with complex operations, public agencies, infrastructure companies, private companies, or companies already using ISO 14001 or other ISO management systems.

ISO 14060 may also be useful where the challenge is not only “what should our target be?” but “how do we build the governance, controls, transition plan, documentation, and accountability needed to deliver it?”

For companies preparing climate transition plans under regulatory or investor pressure, ISO 14060 could become a practical bridge between climate strategy, enterprise risk management, environmental management systems, and disclosure readiness.

Why Companies May Need Both ISO 14060 and SBTi

For many years, net zero commitments were largely voluntary. Companies adopted science-based targets, published sustainability reports, and announced ambitious climate goals in response to investor expectations, customer pressure, and corporate values. Today, however, climate commitments are increasingly intersecting with mandatory disclosure requirements.

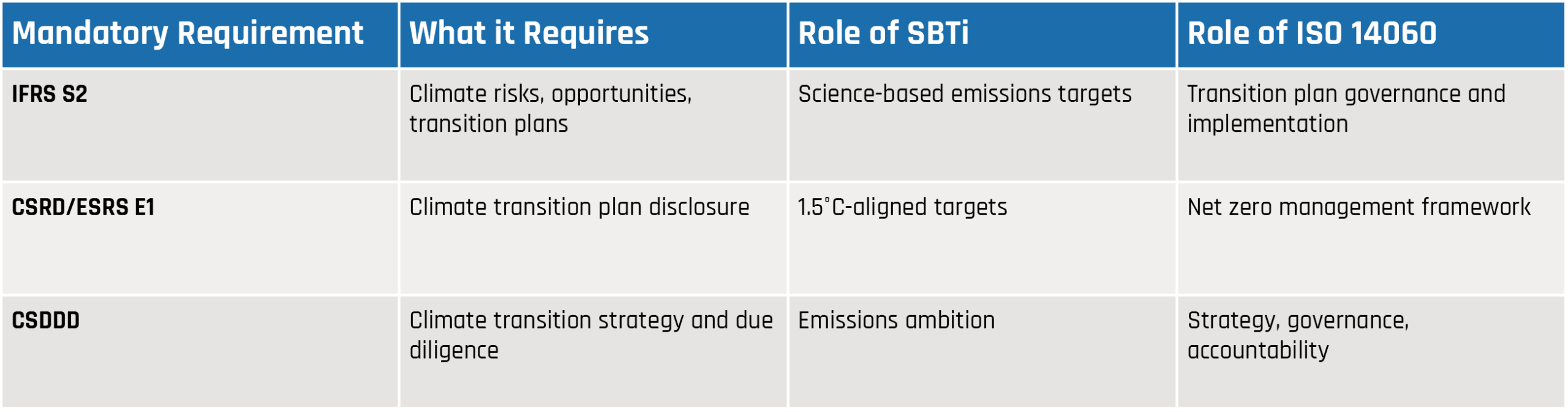

Frameworks such as the International Sustainability Standards Board’s (ISSB) IFRS S2 Climate-related Disclosures and the European Union’s Corporate Sustainability Reporting Directive (CSRD), implemented through the European Sustainability Reporting Standards (ESRS), require companies to disclose not only their greenhouse gas emissions and targets, but also the governance, strategy, risks, transition plans, and resources supporting those commitments. [5]

This shift raises an important question: How can companies demonstrate that their net zero ambitions are credible, actionable, and embedded within business operations?

The answer may lie in combining the strengths of SBTi and ISO 14060. SBTi provides external credibility for emissions reduction targets. It establishes whether a company’s near-term and long-term greenhouse gas reduction goals are aligned with climate science and SBTi’s applicable target-setting methodologies. Investors, customers, and rating organizations increasingly recognize SBTi validation as a benchmark for ambition and target credibility. [3]

ISO 14060 addresses a different challenge. It provides a framework for developing and maintaining the systems required to achieve those targets. This includes governance structures, organizational accountability, transition planning, implementation processes, monitoring, and continual improvement. In essence, ISO 14060 may provide the operational architecture behind a company’s net zero strategy.

While SBTi and ISO 14060 were developed as voluntary frameworks, their importance is growing as climate disclosure requirements become increasingly mandatory. As a result, many organizations are beginning to view these standards not simply as sustainability tools, but as building blocks for regulatory compliance and disclosure readiness.

IFRS S2: Connecting Net Zero Commitments to Investor Disclosures

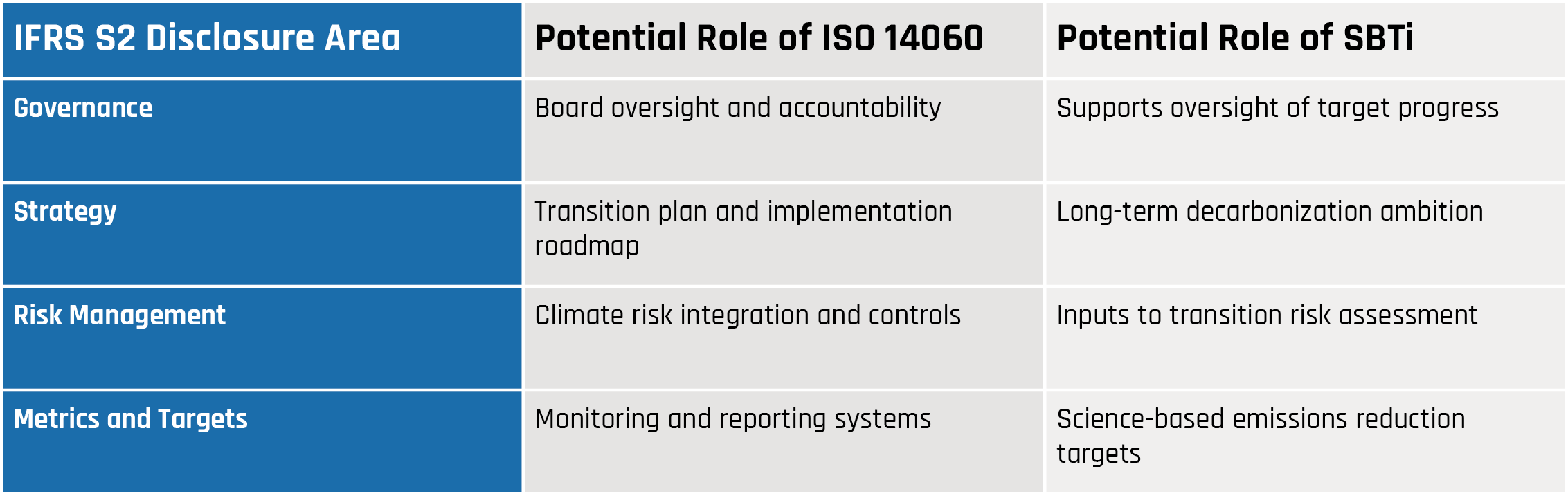

IFRS S2 requires companies to disclose climate-related information across four pillars:

- Governance

- Strategy

- Risk Management

- Metrics and Targets

ISO 14060 could provide the supporting management system for these disclosures, while SBTi provides the validated targets disclosed under the Metrics and Targets pillar. [5]

A company may therefore disclose:

“Our net zero transition plan is developed in accordance with ISO 14060 principles for Net Zero Aligned Organizations, and our greenhouse gas reduction targets have been independently validated by the Science Based Targets initiative.”

ESRS E1: From Climate Commitments to Transition Plans

The European Sustainability Reporting Standards go even further. ESRS E1 requires organizations to disclose [6]:

- A climate transition plan

- Decarbonization levers and actions

- Climate governance

- Policies and targets

- Capital expenditures aligned with the transition

- Progress toward climate goals

ISO 14060 is particularly well aligned with these requirements because its primary focus is establishing the systems, governance, and implementation pathways needed to deliver net zero commitments. Meanwhile, SBTi can provide confidence that the emissions reduction pathway embedded in the transition plan is grounded in climate science.

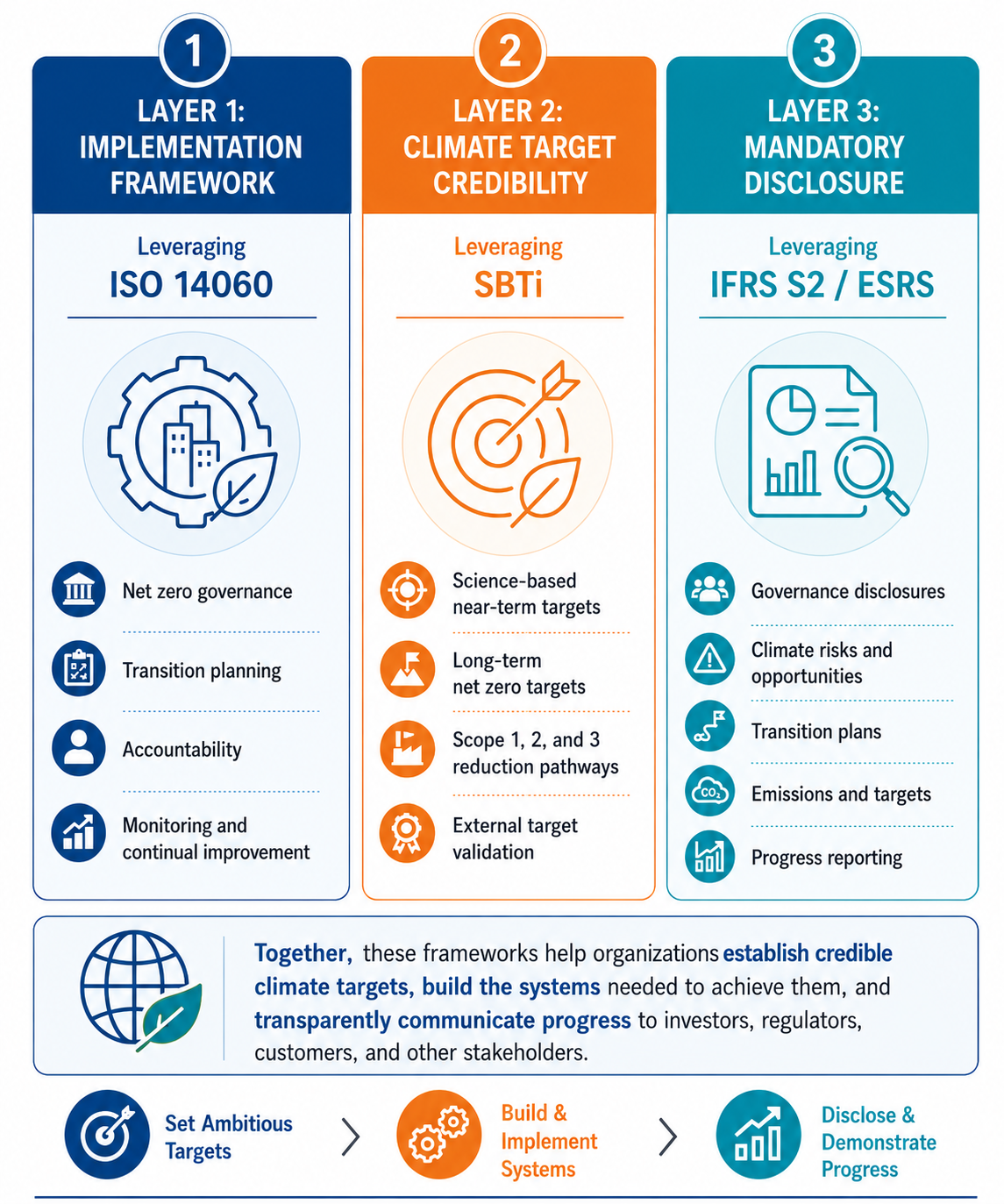

The Emerging Climate Accountability Stack

As mandatory reporting expands globally, many organizations may adopt a three-layer approach that helps organizations move from climate ambition to implementation, verification, and transparent disclosure:

Viewed together, these frameworks illustrate how climate management is evolving from a focus on target-setting toward a more integrated model of implementation, validation, and disclosure. SBTi establishes where a company needs to go, and ISO 14060 helps define how it gets there. IFRS S2 and ESRS provide the framework for transparently communicating that journey to investors, regulators, and stakeholders.

As climate reporting evolves from voluntary commitments to mandatory accountability, companies that can integrate all three elements, credible targets, robust implementation systems, and transparent disclosure, may be best positioned to demonstrate both ambition and execution.

IFRS S2 | CSRD/ESRS EI | CSDDD

IFRS S2 | CSRD/ESRS EI | CSDDD

Criticisms of SBTi

SBTi’s influence has also made it a target of criticism. Some critics argue that Version 2.0 introduces too much flexibility and weakens the rigor that made SBTi valuable. Recent reporting has highlighted concerns that the revised standard allows companies to miss targets if they demonstrate “best efforts,” disclose barriers, and provide evidence of action. Critics have also raised concerns about greater flexibility around energy certificates and value chain approaches. [8]

SBTi has also faced scrutiny over governance, corporate influence, and sector-specific standards. Its oil and gas standard was reportedly paused after several major energy companies withdrew from the process, raising questions about how voluntary standards should handle hard-to-abate and fossil-fuel-intensive sectors. [9]

The central criticism is that if SBTi becomes too flexible, it risks losing scientific credibility. If it remains too strict, some companies may disengage. Version 2.0 is an attempt to navigate that tension.

Criticisms of ISO 14060

Because the standard is new and still in consultation [1], it remains to be seen how rigorous, auditable, and widely adopted it will be. ISO standards can be powerful because they are globally recognized, but they can also be broad. If ISO 14060 becomes too process-oriented, it may help companies document net zero plans without necessarily ensuring the level of emissions reductions needed for climate alignment.

Another concern is that companies may use ISO alignment as a credibility signal without pursuing SBTi-level emissions reduction ambition. The effectiveness of ISO 14060 will depend heavily on the final requirements, assurance practices, and how clearly it addresses offsets, residual emissions, Scope 3 emissions, and transition plan accountability. [7]

Final Thoughts: The Future of Net Zero Is Integration

For more than a decade, corporate climate action has focused on setting commitments. The next decade will be defined by an organization’s ability to demonstrate implementation, accountability, and measurable progress.

As regulators, investors, customers, and lenders increasingly seek evidence of credible transition planning, organizations will need more than ambitious targets alone. They will need governance structures, management systems, implementation roadmaps, performance monitoring, and transparent disclosure mechanisms capable of supporting long-term climate commitments.

Viewed through that lens, SBTi, ISO 14060, IFRS S2, and ESRS are not competing frameworks. They address different dimensions of the same challenge.

- SBTi helps establish whether targets are scientifically credible.

- ISO 14060 helps organizations build the systems needed to achieve them.

- IFRS S2 and ESRS provide the disclosure framework for communicating progress and accountability to investors and stakeholders.

Organizations that successfully integrate all three approaches may be better positioned to demonstrate not only climate ambition, but climate execution. As climate reporting continues to mature, organizations will increasingly be judged not only on the ambition of their commitments, but on the credibility of their pathways and the transparency of their progress. The question is no longer simply “What is your target?” The more important question is becoming “How will you deliver it and how will stakeholders verify your progress?”

REFERENCES

1. International Organization for Standardization (ISO). IWA 42:2022 Net Zero Guidelines. Available at: ISO IWA 42 Net Zero Guidelines

2. International Organization for Standardization (ISO). ISO launches international standard for net zero alignment. June 2026. Available at: ISO Net Zero Alignment News

3. IFRS S2 Climate-related Disclosure. Available at: IFRS S2 Climate-related Disclosures

4. Science Based Targets initiative (SBTi). Corporate Net-Zero Standard Version 2.0. Available at: SBTi Corporate Net-Zero Standard V2

5. Science Based Targets initiative (SBTi). Developing the Net-Zero Standard. Available at: SBTi Net Zero Development Process

6. United Nations Race to Zero Campaign. Starting Line and Minimum Criteria. Available at: UN Race to Zero Criteria

7. International Energy Agency (IEA). Net Zero by 2050: A Roadmap for the Global Energy Sector. Available at: IEA Net Zero Roadmap

8. Financial Times. “Science Based Targets initiative softens climate rules amid criticism.” June 2026. Available at: Financial Times coverage of SBTi revisions

9. Financial Times. “Corporate climate target setter faces criticism over governance and standards.” Available at: Financial Times SBTi governance article

10. European Union. Corporate Sustainability Due Diligence Directive (CSDDD). Directive (EU) 2024/1760. Available at: https://eur-lex.europa.eu/eli/dir/2024/1760/oj