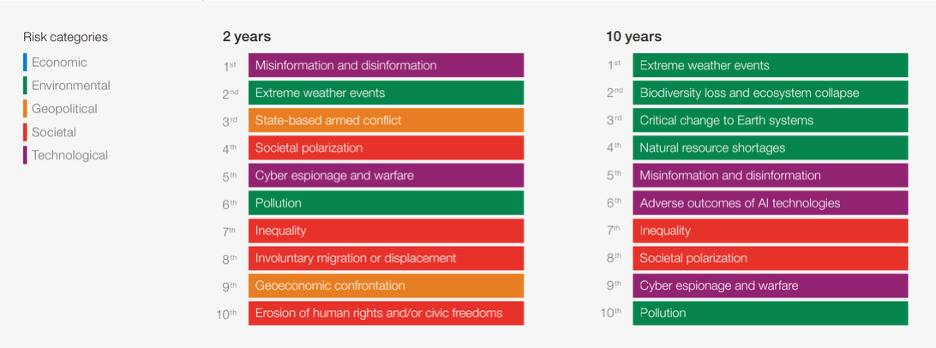

We are approaching the midpoint of 2025, and the global landscape is becoming more uncertain and unstable—geopolitical, environmental, societal, economic, and technological risks are becoming more complex and urgent. Climate-related financial risk management is highlighted in the World Economic Forum’s 2024-2025 Global Risk Perception Survey, which gathers insights from over 900 experts around the world. The report analyses global risks through three timeframes to support decision makers in balancing current crises and longer-term priorities. Environmental risks associated with extreme weather events are considered to have the second-highest material impact—trailing only armed conflict at the present time horizon, and misinformation over the next two years. These environmental impacts are expected to intensify over the next decade (see Fig. 1).

Figure 1. Global risks ranked by severity over the short and long term. Source: World Economic Forum Global Risks Perception Survey 2024-2025.

Extreme weather events already have huge impacts on local, national and global economies. Hurricane Helene, which struck the southeastern United States in late September 2024, had a profound impact on both regional and national economies. It is estimated that the total U.S. economic losses from the hurricane are between $225 billion and $250 billion. While the national GDP impact was relatively modest, the hurricane’s effects were significant in specific sectors and regions. For example, supply chain disruptions led to temporary halts in vehicle production at major facilities, affecting employment and output in those areas. The hurricane’s effects on infrastructure, businesses and reginal economies highlight the need for enhanced resilience and preparedness strategies.

It’s no surprise that investors and regulators worldwide have come to agree on the importance of climate-related financial risk reporting (Fig. 2). The California Senate Bills 253 and 261, amended to 219, reflect this global momentum. CA SB 261 references the TCFD recommendations, which for clarification were disbanded in 2023 and fully incorporated into the International Sustainability Standards Board (ISSB) IFRS S1 – General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 – Climate-related Disclosures (thus standardizing what was previously guidance in TCFD). Both IFRS S2 and TCFD require companies to disclose the processes and policies used to identify, assess, and manage climate-related risks (we will be sharing a detailed comparison between TCFD, IFRS S2 and other international mandates in the coming weeks). Investors want companies to disclose under TCFD/IFRS S2 to help them make informed, long-term investment decisions. While many jurisdictions have adopted IFRS S2, some like CA SB 261, reference TCFD as a foundation for climate reporting, either due to ongoing transitions or continued recognition of TCFD’s importance.

Figure 2. Global momentum of climate-related disclosures. According to the most recent IFRS Report, over 30 jurisdictions represent 57% of global GDP, more than 40% of global market capitalization, and more than half of global greenhouse gas emissions, have already finalized decisions on the adoption or other use of ISSB Standards, or are making progress to adopt or otherwise use the standards.

At GSI, we work with companies across various industries that may not have previously considered how to integrate climate-related risks—like physical risks (e.g., extreme weather) and transition risks (e.g., carbon regulations)—into their broader risk management processes. Fortunately, many companies already have established risk management processes in place, making it easier to integrate climate-related risks into these systems rather than developing a completely new process.

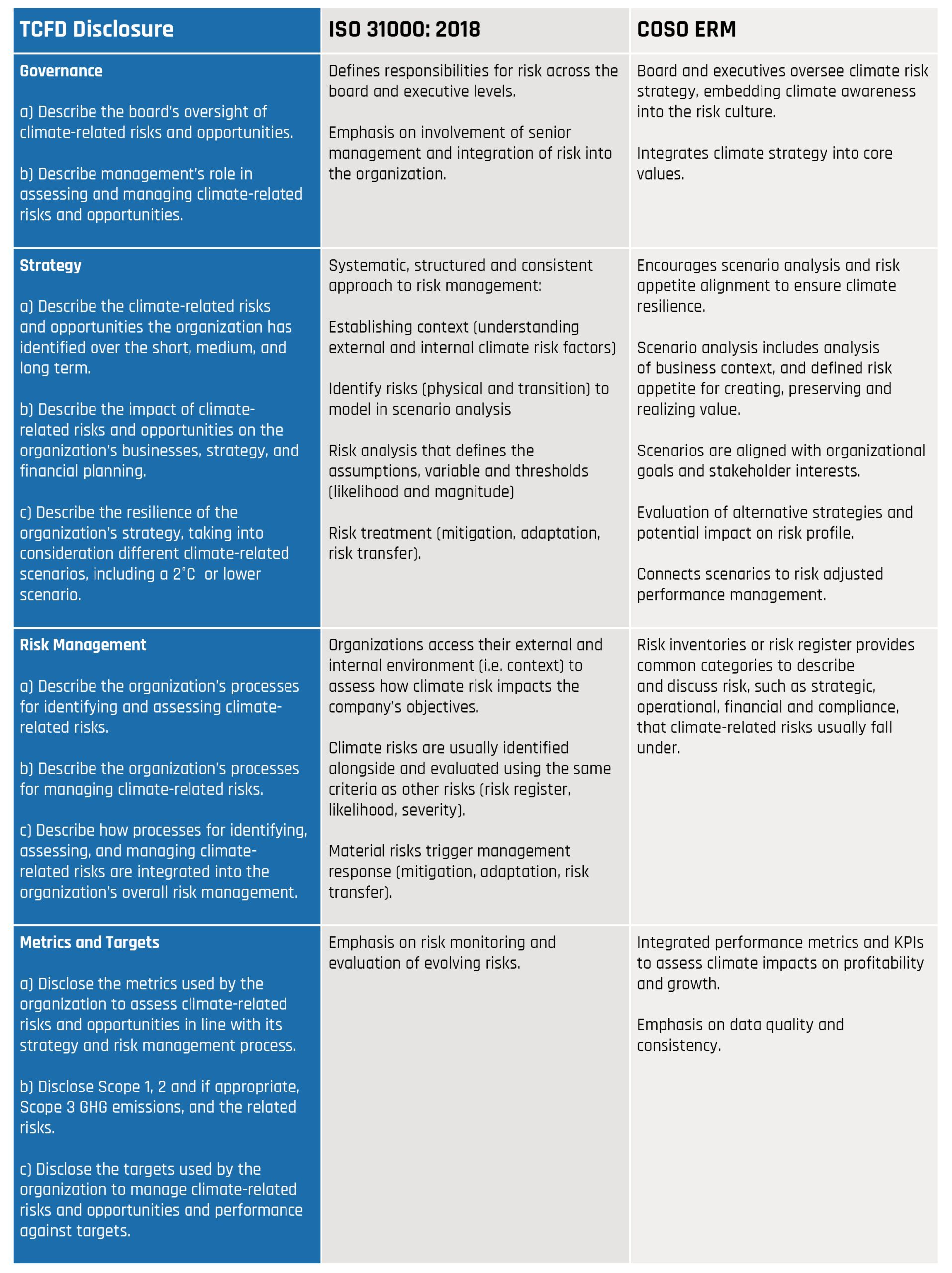

Whether a company already has a risk management system in place or is considering implementing one, ISO 31000, the international standard for risk management, and COSO ERM (Enterprise Risk Management) offer well-established, recognizable, and credible processes to build upon. ISO 31000 provides a structured and adaptable methodology for identifying, assessing, and treating risks, including those related to climate change. The COSO ERM Framework provides a strategic and integrated approach to risk management that is well-suited to support climate risk assessment. While not climate-specific, COSO’s emphasis on governance, strategy alignment, and performance makes it a powerful tool for embedding climate risk into broader enterprise planning—especially when conducting scenario analysis. By integrating climate risk and scenario planning with a standardized risk management system, companies can align these processes with their existing strategic planning cycles, helping to inform corporate, business, and functional strategies. To make the case for integration, GSI, we have summarized the synergy between the TCFD Disclosure, ISO 31000, and COSO ERM in Table 1 below.

Table 1. Synergies between existing risk management principles We increasingly see and encourage clients to consider implementing or reference existing ISO 31000 or COSO ERM in their climate disclosures. For example, a multinational company might say something like “Our enterprise risk management approach follows ISO 31000 principles, and climate-related risks are integrated into this framework through structured risk identification, evaluation and treatment processes” or “Our risk governance aligns with the COSO ERM to ensure climate risks are integrated into the company’s strategic outlook.” They may highlight how climate risk is embedded into their risk register, or the roles of risk owners and governance committees.

We increasingly see and encourage clients to consider implementing or reference existing ISO 31000 or COSO ERM in their climate disclosures. For example, a multinational company might say something like “Our enterprise risk management approach follows ISO 31000 principles, and climate-related risks are integrated into this framework through structured risk identification, evaluation and treatment processes” or “Our risk governance aligns with the COSO ERM to ensure climate risks are integrated into the company’s strategic outlook.” They may highlight how climate risk is embedded into their risk register, or the roles of risk owners and governance committees.

As global risks continue to intensify, integrating climate-related risks into existing risk management systems is more crucial than ever. By aligning climate risk with established frameworks like ISO 31000 and COSO ERM, companies can take meaningful steps to incorporate climate considerations into their broader strategic planning, ensuring resilience and long-term success. If companies are not able to implement ISO or COSO, we are still able to use the frameworks and concepts to make our client’s risk management processes more robust. Ultimately, disclosing climate-related risks helps companies build credibility, demonstrating that their processes are well-structured, globally recognized, and aligned with best practices in sustainability and governance, all while enhancing their ability to manage the most significant risks facing their business today and in the future.

If this information is useful to you or you have questions about climate-related financial risk management or how to start integrating climate into your existing processes, please feel free to reach out. Our team has decades of combined experience and is able to support all aspects of CA SB 219 compliance.