Global momentum of Climate Disclosures

While some of our clients are new to climate reporting, it is important to understand that California climate disclosure laws are not happening in a vacuum – that they align with most other developed economies and regulators. Most sustainability-related disclosure mandates have considerable overlap, meaning that alignment with one regulation often results in alignment or partial alignment with another one. Understanding the key similarities and differences in these reporting standards will help organizations improve their reporting efficiency and meet stakeholder and regulatory demands. Ultimately, the goal is to streamline compliance-based reporting so that companies can focus on strategy and value creation.

How does CA SB 219 compare to other global climate mandates?

CA SB 219 is part of the California Climate Accountability Package, which includes SB 253 and SB 261 – which were amended by SB 219. CA SB 219 requires companies to disclose using the Notably, TCFD was disbanded in 2023 and its functions were fully incorporated into the International Sustainability Standards Board (ISSB) who then drafted IFRS S1 – General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 – Climate-related Disclosures (thus standardizing what was previously guidance in TCFD). IFRS S2 effectively replaces and builds upon the TCFD recommendations.

IFRS S2 brings structure to global climate-related financial risk reporting. The ISSB sustainability reporting requirements have since been enacted by several countries including Australia, Costa Rica, Malaysia, Sri Lanka, Tanzania, Pakistan, and others. Additional jurisdictions such as Canada, China, and Mexico are planning to implement ISSB reporting requirements in the near future (Fig. 1).

Figure 1. The latest IFRS Report shows that more than 30 jurisdictions (together accounting for 57% of global GDP, over 40% of market capitalization, and more than half of worldwide greenhouse gas emissions) have either finalized their plans to adopt ISSB Standards or are actively moving toward their use.

During Senator Weiner reiterated the Senate Bill would align with other global reporting mandates and standards, however he did not state explicitly that IFRS S2 would be a satisfactory reporting standard.

How does TCFD compare to IFRS S1 and S2 Disclosure Requirements?

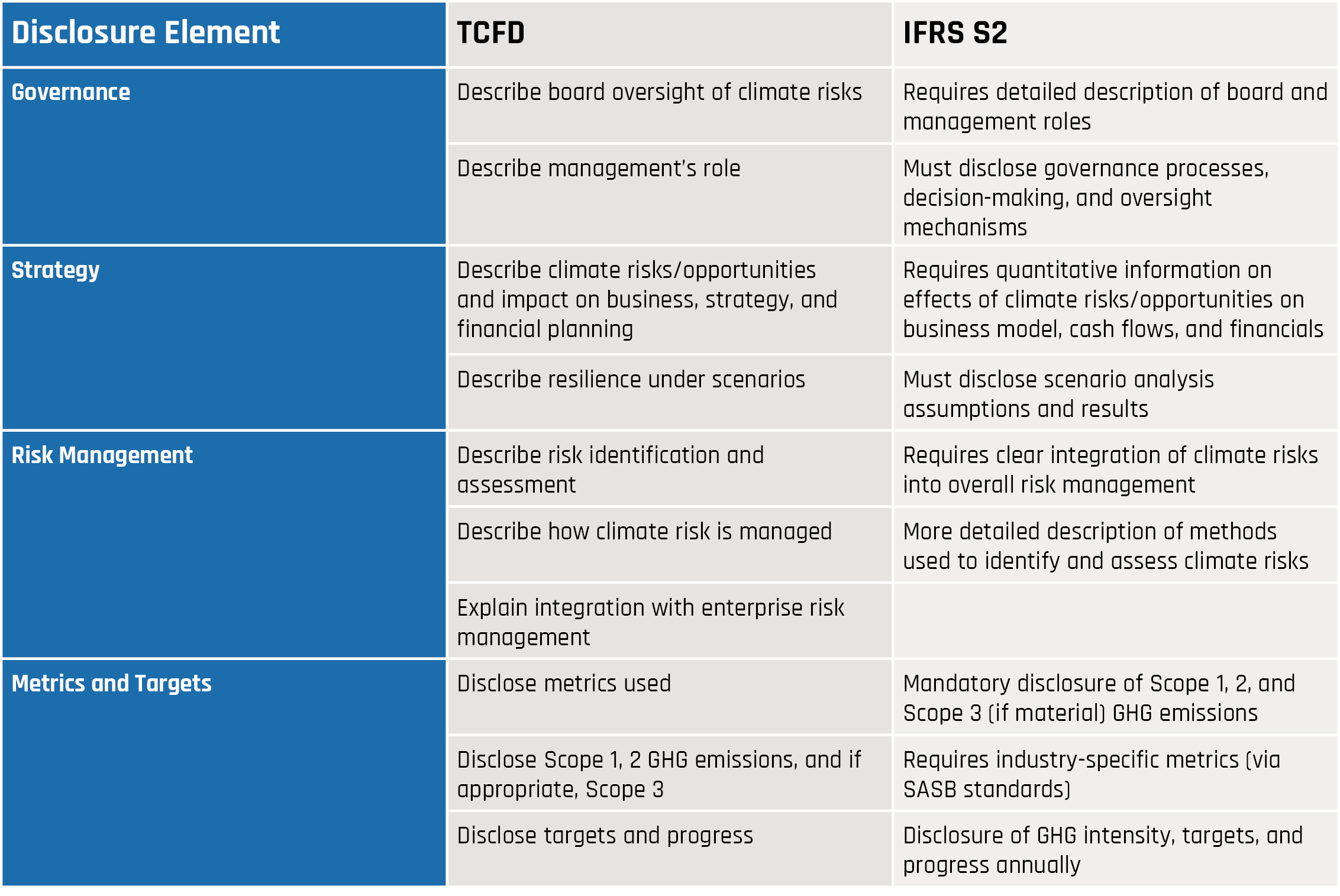

Both the ISSB sustainability standards and TCFD require companies to disclose climate-related financial impacts from a financial materiality perspective, which examines how climate-related risks and opportunities impact a company’s financial performance (such as revenues, cash flows and asset valuations). The disclosure requirements in IFRS S2 significantly build upon the framework established by TCFD, with increasing attention and detail on financial materiality (Table 1).

Table 1. Comparison of disclosure requirements in TCFD and IFRS S2.

In particular, IFRS S2 requires more detailed descriptions of the process for identifying and assessing climate related risks, emphasizing the importance of conducting a climate scenario analysis (CSA).

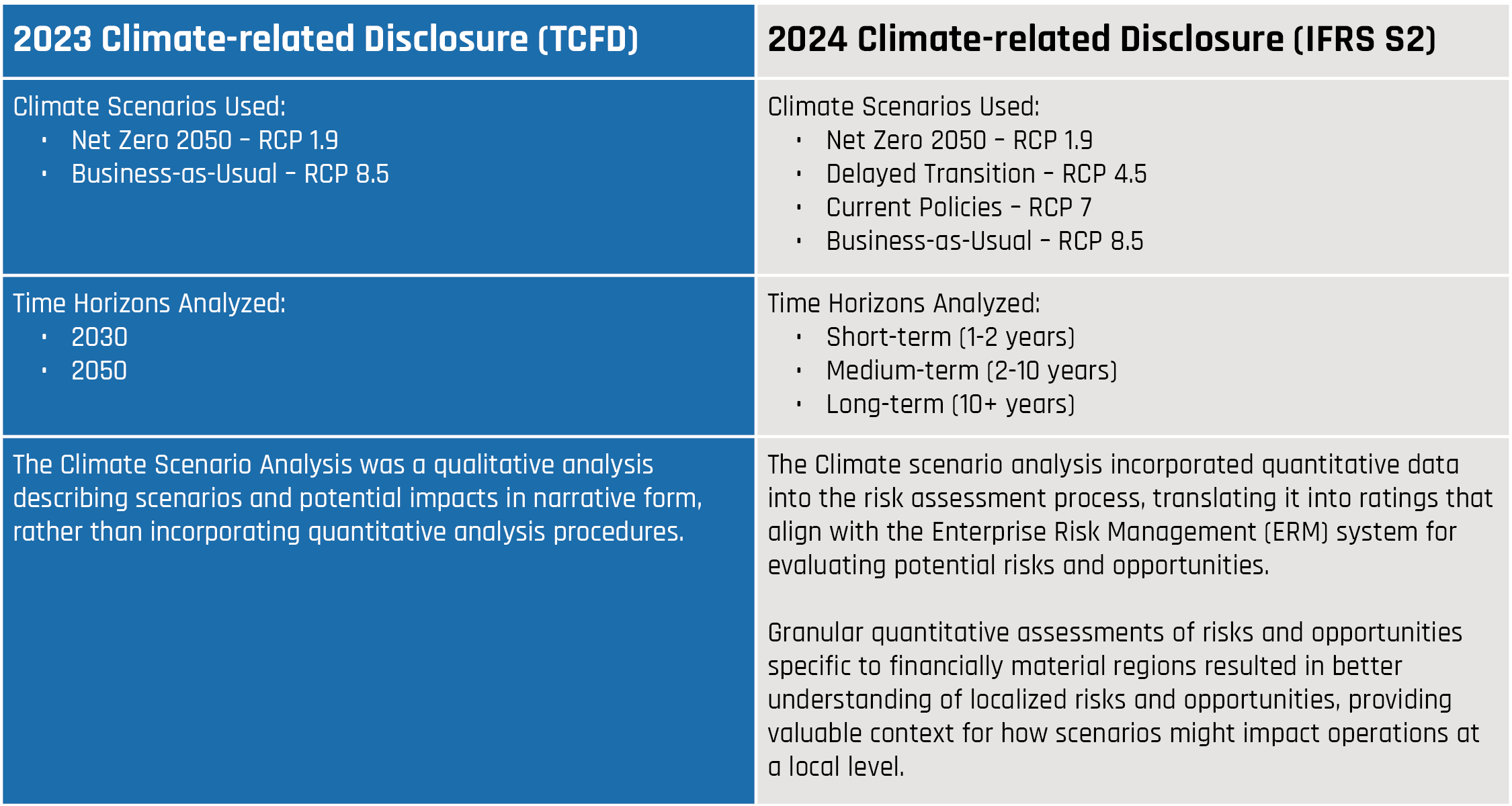

Companies are adjusting their reporting to the changes from TCFD to IFRS accordingly. GSI analyzed public disclosures and found particularly useful examples of the shift from TCFD to IFRS with Wheaton Precious Metals, a Canadian precious metals corporation that primarily sells gold and silver in North America, Europe, Africa, and South America. Wheaton voluntarily reported climate-related disclosures aligned to TCFD in 2022 and 2023. In 2024, Wheaton Precious Metals began reporting their climate-related disclosures aligned to IFRS S2 requirements to meet Canada’s Canadian Sustainability Disclosure Standards (CSDS 1 & CSDS 2) regulatory requirements. The 2024 climate-related disclosures reported to the IFRS S2 significantly build on Wheaton Precious Metals’ previous TCFD disclosures (Table 2).

Table 2. Major differences between Wheaton Precious Metals TCFD-aligned climate-related disclosure from 2023 and their IFR S2-aligned disclosure from 2024.

2023 Climate-related Disclosure (TCFD)

2024 Climate-related Disclosure (IFRS S2)

How does CA SB 219 compare to the EU’s CSRD?

Both California’s Senate Bill 219 and the European Union’s Corporate Sustainability Reporting Directive (CSRD) are key pieces of legislative packages aimed at improving corporate transparency, consistency and quality of climate-related risks and impacts. They are designed to inform investors, regulators and the public about how companies affect and are affected by the environment and social factors. While both CA SB 219 and CSRD align or build upon global reporting standards (TCFD and the GHG Protocol), there are a few key differences.

Differences in Focus Area: CA SB 219 requires companies to disclose climate-related matters only, whereas the European Sustainability Reporting Standards (ESRS) developed for CSRD compliance cover a broad range of environmental, social and governance matters.

It is worth noting that CSRD fully incorporates IFRS S2 disclosure requirements for climate-related disclosures, meaning that companies disclosing CSRD’s climate standard will meet California’s disclosure requirements.

Differences in the Definition of Materiality: CA SB 219 only requires organizations to consider materiality from a financial perspective. Under CA SB 219, all in-scope entities are required to report on Scope 1, 2, and 3 emissions, regardless of materiality. CSRD on the other hand, requires organizations to complete a double materiality assessment (evaluating both impact and financial materiality) and disclose set of ‘General Disclosures’ that cover key sustainability reporting aspects such as governance frameworks, strategy disclosures, and impact management.

In addition, CSRD requires more detailed climate-related information if it is deemed to be material such as metrics on energy consumption, mix, and intensity.

Differences in Scope: CA SB 219 mandates that US-based companies operating in California disclose certain sustainability information. Companies with annual revenues of $1 billion or more must publicly disclose their Scope 1 and Scope 2 emissions starting in 2026, followed by Scope 3 emissions in 2027. Additionally, companies with annual revenues exceeding $500 million are required to disclose climate-related financial risk reports beginning in 2026 with biannual updates.

The EU’s CSRD requires EU-based companies with 250+ employees and at least €50 million in net turnover or a balance sheet exceeding €25 million to disclose sustainability information using applicable ESRS standards. Non-EU-based companies that generate €150 million in net turnover annually within EU member states are also subject to CSRD reporting.

Differences in Disclosure: CA SB 219 requires a greenhouse gas inventory for Scope 1, 2 and ultimately Scope 3 emissions, as well as an aligned Climate-Related Financial Risk Report. CSRD requires detailed disclosures using the European Sustainability Reporting Standards (ESRS), which are aligned with TCFD, as well as GRI and SASB/ISSB IFRS S2.

Differences in Third-party Assurance: CA SB 219 requires limited assurance for Scope 1 and 2 emissions data beginning in 2026 with requirements for reasonable assurance beginning in 2030. Scope 3 emissions data will need limited assurance starting in 2027. There is no escalation of the assurance to reasonable assurance for Scope 3 emissions under CA SB 253. Additionally, there are no third-party assurance requirements for TCFD-aligned climate-related disclosures under CA SB 261.

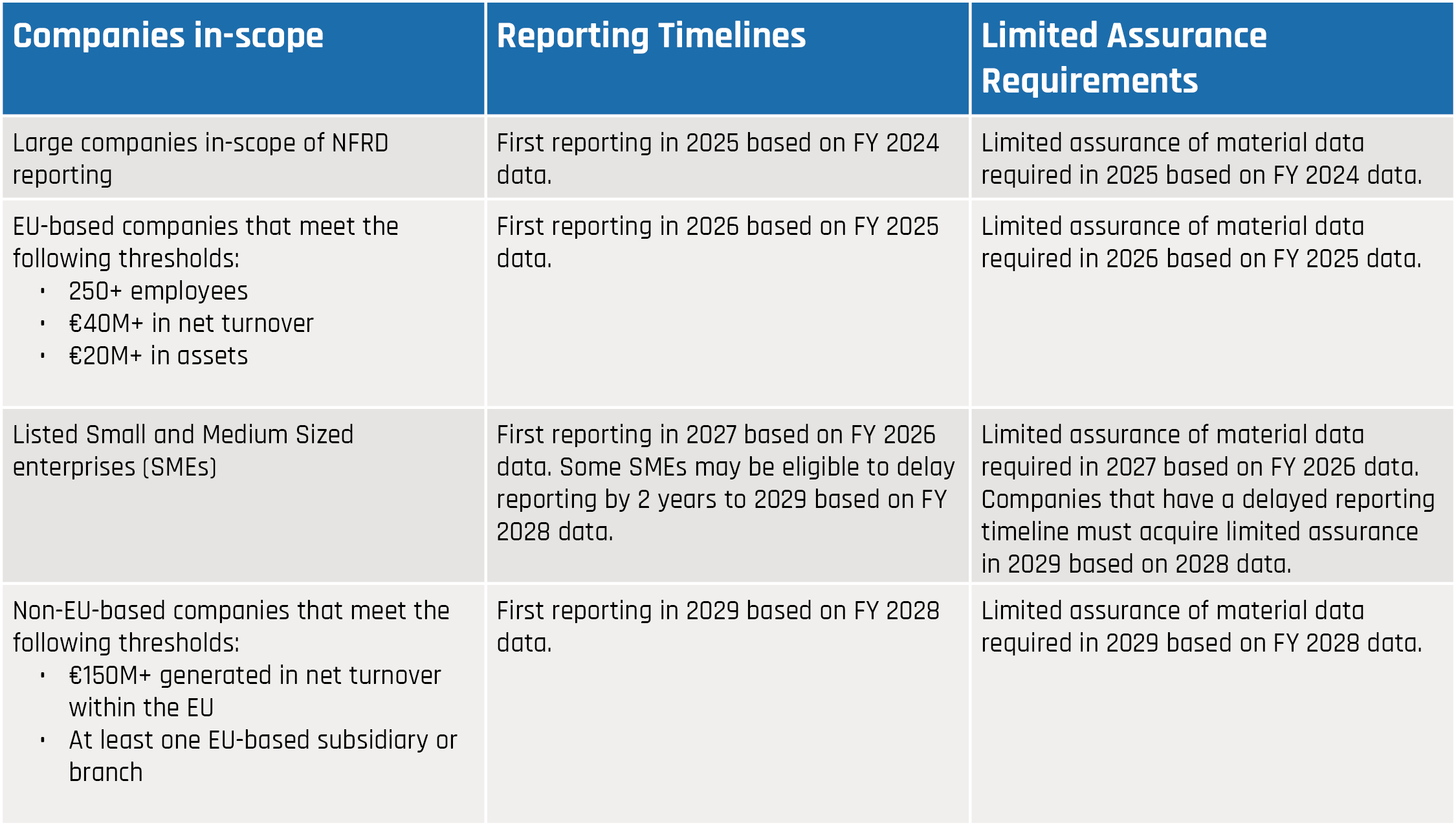

Under CSRD, limited assurance verification procedures are being introduced gradually, aligning to the timelines that correspond to the phased-in implementation for in-scope reporting companies (Table 3). Data assurance is required for all sustainability topics (environmental, social, governance) that have been deemed material through the Double Materiality Process. The European Commission is currently determining if it is feasible to require companies to transition to obtaining reasonable assurance for their sustainability data. The Commission is expected to assess the feasibility of reasonable assurance and adopt corresponding standards no later than October 2028.

Table 3. Phased-in reporting timelines for CSRD data as well as the limited assurance requirement timelines for companies in scope of CSRD reporting.

Differences in Enforcement: CA SB 219 will be enforced by the California Air Resources Board (CARB). In 2024, CARB announced that they will not administer penalties for incomplete Scope 1 and Scope 2 data reported in 2026 as they do not expect all in-scope companies to be fully compliant with the regulations in the first year of reporting. Under CA SB 219, penalties for non-compliance with GHG emission requirements can result in fines of up to $500,000 per reporting year. CARB is expected to adopt final regulations and detail how they will enforce the legislation by July 1, 2025.

Enforcement of CSRD and penalties for non-compliance are handled at the member-state level. Each EU member-state is responsible for translating the CSRD into their national legislature and for ensuring compliance by in-scope entities. Member states can adjust the legislature to fit the needs of their individual country. Although penalties differ by country, non-compliance may lead to fines and penalty fees, legal actions against the company such as audits, investigations, and lawsuits, reputational harm, and in France, potentially even imprisonment for company directors if the non-compliance is considered severe enough.

What are other jurisdictions doing?

As mentioned above, there are over 35 other jurisdictions with proposed or enacted climate reporting mandates. The ISSB standards have been modified in the jurisdictions where they were adopted to reflect local data collection and aggregation methodologies, provide companies with phased-in adoption timelines if necessary, and customize reporting requirements to governmental agencies established standards.

United Kingdom

While the United Kingdom has plans to implement ISSB standards starting in 2026, there are already mandatory sustainability standards in place, namely, the United Kingdom Sustainability Reporting Standards (SRS). These standards are based on the ISSB IFRS S1 and S2 frameworks but have not yet been fully implemented. To facilitate a smoother transition for companies in adopting the full IFRS S1 and S2 standards, organizations subject to the SRS have been mandated to publish TCFD disclosures annually starting in 2022. The range of companies in scope of SRS mandates is narrower than the requirements set by standards such as CA SB 219 and CSRD. The UK SRS is only applicable to companies listed on the United Kingdom Stock Exchange. The scope of companies subject to SRS reporting may increase to include SMEs and privately held firms in the future.

New Zealand

New Zealand developed their own climate-related disclosure standards called the Climate-Related Disclosures Regime in 2023 with the help of the External Reporting Board. Climate disclosures are a key legislative piece of the Financial Sector Climate-related Disclosures act which requires certain entities such as large financial institutions, insurers, and listed companies to report climate-related information such as governance structures and risk management frameworks for addressing and managing climate-related risks, climate-related strategy impacts, and greenhouse gas emission data.

The New Zealand climate standards were developed in tandem with the ISSB IFRS S1 and S2 standards to ensure compatibility. However, the New Zealand standards include a strong emphasis on incentivizing partnerships with indigenous Māori tribes and feature phased-in adoption compliance to ease the reporting burden on smaller firms. New Zealand’s Climate-Related Disclosures Regime focuses on the financial sector whereas CA SB 219 and other jurisdictions adoptions of ISSB IFRS S1 and S2 standards applies to a broader range of companies and industries.

Australia

The Australian Sustainability Reporting Standards (ASRS) have adapted IFRS S1 to make their voluntary ASRS 1 standard for general sustainability-related disclosures and IFRS S2 to their mandatory ASRS 2 standard for their climate-related financial disclosures. Alongside making one standard voluntary and the other mandatory, there are a few key differences between the IFRS S1 and S2 standards and the ASRS 1 and 2 standards.

- ASRS 2 does not require industry-based metrics or reference SASB standards, as the IFRS S2 standard does. We have not discussed industry-based standards in this article, but it is worth mentioning the additional disclosures some industries are required under IFRS S2 (particularly those in financial sectors). CARB has not indicated if companies are required to follow the TCFD industry specific guidance to date.

- ASRS 2 is applicable to both for-profit and nonprofit organizations whereas the IFRS S2 standard is only applicable to for-profit entities.

- ASRS 2 requires organizations to undertake two mandatory climate scenarios – one consistent with 1.5°C of warming and one high emissions scenario that well exceeds 2°C of warming. The IFRS S2 standard only requires organizations to provide analysis on climate scenarios that are aligned with the entity’s particular circumstances – there are no specific climate scenarios the IFRS requires organizations to use.

Conclusion

The global sustainability reporting landscape is changing daily as regulators balance the need to protect the climate and inform the public, while ensuring that businesses remain competitive globally. While the current state of reporting may seem fragmented, there is an increasing effort across the world to unify requirements to make them more comparable across countries and reduce the number of burdens that companies face when complying.

At GSI, we are monitoring these changes closely to ensure that our clients are well prepared for the future of sustainability reporting. If your organization has questions about what regulations might apply to you or how your current reporting meets these standards, please reach out to us and we would be happy to discuss.