SB 219 Compliance California

California has long been at the forefront of national environmental and climate policy, setting ambitious goals for reducing GHG emissions and promoting sustainable initiatives. With the passage of Senate Bills 253 and 261, further amended by Senate Bill 219, the state is implementing one of the most significant climate disclosure frameworks in the United States. These laws, scheduled to be in effect January 1, 2026, require thousands of public and private companies to disclose detailed information about their greenhouse gas (GHG) emissions and climate-related financial risks. For companies that do business in California, understanding the implications of this legislation is critical for compliance, risk management, and long-term planning.

This is the first of a multi-part series of articles that GSI will publish over the next several months. The series will provide an overview of the California climate legislation, highlight key concerns and recommendations raised during the public comment process, and offer guidance on how businesses can prepare for successful implementation. We will also take a global look at how California climate disclosures align with those in other jurisdictions and give our thoughts on the process of Climate Risk Assessments and Climate Scenario Analysis. We will wrap up the series after the California Air Resource Board (CARB) releases the final rule.

We will start this series by discussing what these bills hope to accomplish, and their basic requirements.

Overview of Senate Bills 253 and 261, as Amended by SB 219

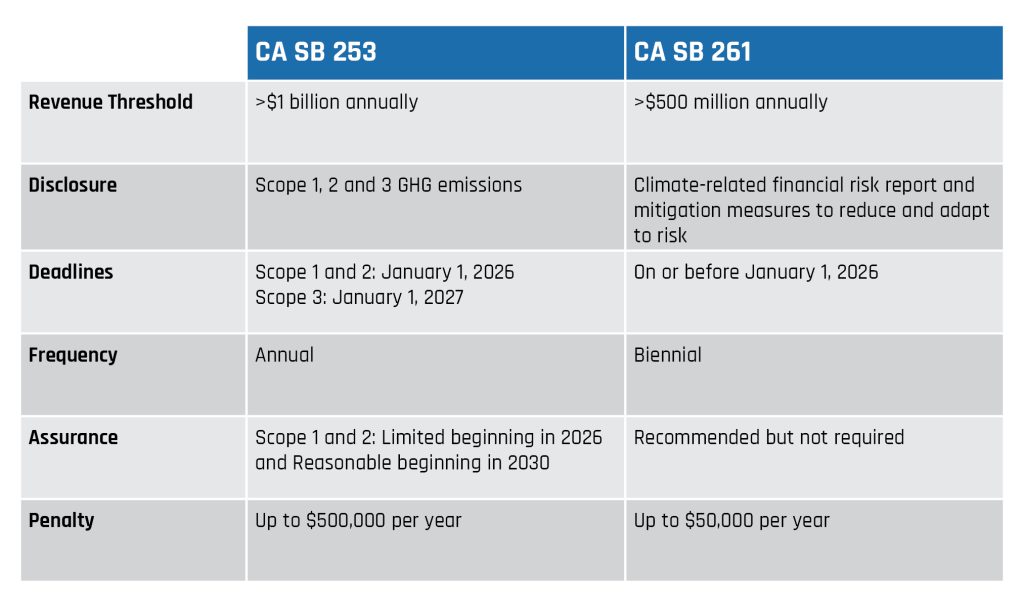

Senate Bill 253 (SB 253): Known as the Climate Corporate Data Accountability Act, SB 253 requires companies with annual revenues over $1 billion and doing business in California to publicly disclose their full GHG emissions, including Scope 1 (direct emissions), Scope 2 (indirect emissions from purchased electricity), and Scope 3 (all other indirect emissions in a company’s value chain). Reporting must be conducted in accordance with the Greenhouse Gas Protocol and initially subject to third-party limited assurance. The required assurance level for Scope 1 and Scope 2 emissions disclosures potentially increases to a reasonable assurance level in 2030.

Senate Bill 261 (SB 261): Referred to as the Climate-Related Financial Risk Disclosure Act, this bill mandates that companies with annual revenues over $500 million doing business in California prepare biennial reports detailing their climate-related financial risks and the strategies they employ to mitigate these risks. These disclosures must align with the Task Force on Climate-related Financial Disclosures (TCFD) framework.

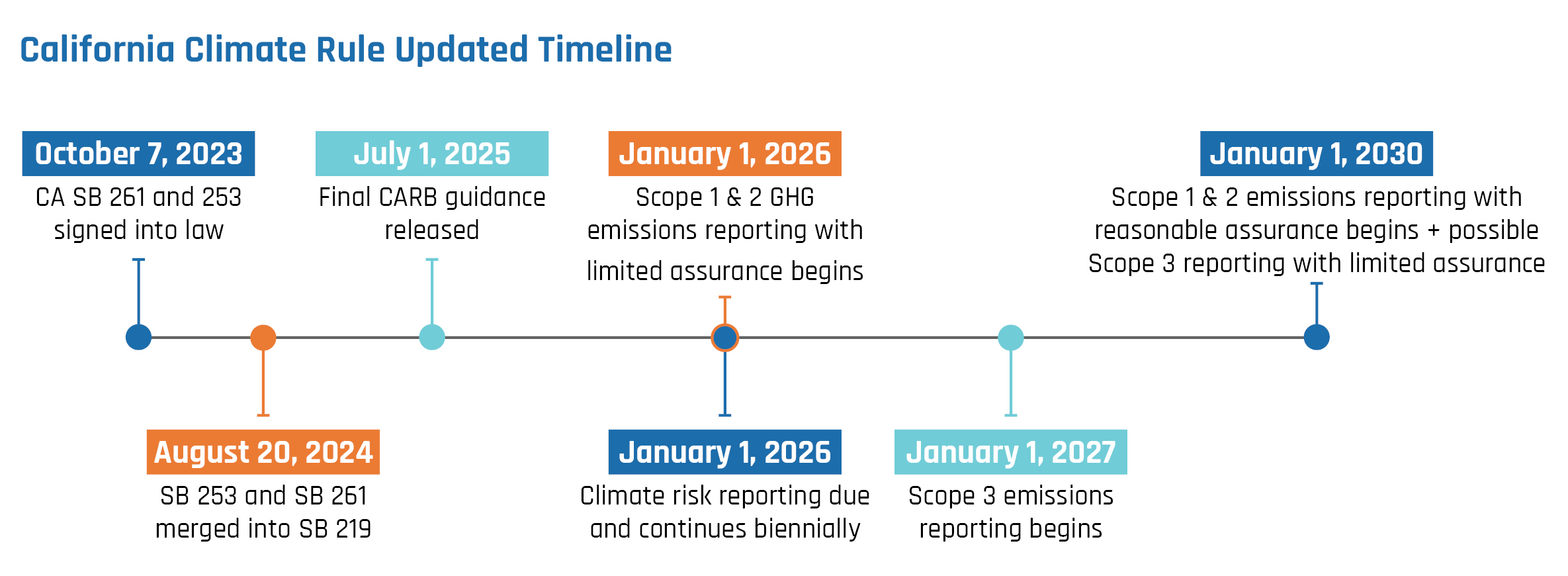

Senate Bill 219 (SB 219): SB 219 amends SB 253 and SB 261 to address implementation challenges and better incorporation of stakeholder feedback. Notable amendments include clarifications on compliance timelines, improved alignment with federal and international standards, and greater specificity around agency responsibilities and data reporting formats. Of most interest to reporting companies is that:

- SB 219 extends the deadline for CARB to develop and adopt regulations for GHG emissions reporting from January 1, 2025, to July 1, 2025.

- Scope 3 emissions reporting for CA SB 253 is delayed until 2027 (originally 2026), recognizing the complexity of collecting upstream and downstream data.

- Companies are allowed to use TCFD-aligned or similar reports (e.g., CDP responses) to satisfy SB 261 reporting, streamlining compliance.

- Consolidated reporting at the parent company level. To further ease the reporting process, SB 291 clarifies that GHG emissions disclosures can be consolidated at the parent company level. This means that subsidiaries are not required to file separate reports if their emissions are included in a comprehensive parent company disclosure.

- New timeline for Scope 3 emissions disclosure. Originally, SB 253 mandated that reporting entities disclose their Scope 3 emissions no later than 180 days after their Scope 1 and Scope 2 emissions disclosures. SB 219 revises this and establishes that there will be a specific schedule for Scope 3 emissions reporting.

Evaluating your current readiness

These bills position California as a national leader in climate transparency and put significant obligations on a wide swath of companies operating in or connected to the state. As California’s SB 219 disclosure requirements move closer towards implementation, companies subject to the law are navigating an evolving landscape—often without clear regulatory guidance. At GSI, we’ve been working closely with clients across sectors to prepare robust, defensible disclosures, grounded in best practices and aligned with international standards. We also have extensive experience in CARB rulemaking for various regulations including AB32 (Global Warming Solutions Act of 2006). From our experience with CARB and sustainability reporting, CA SB 219 reporters generally fall into three categories:

- First-Time Reporters: These organizations are new to climate-related financial risk reporting. While some have foundational elements in place, they are still maturing their programs. For them, SB 219 presents an opportunity to begin articulating how climate risks may impact their operations and to outline plans for improving governance, scenario analysis, and metrics over time.

- Experienced but Evolving Reporters: This group has responded to customer or investor demands in the past through voluntary disclosures (often aligned with frameworks like TCFD), but are now using SB 261 as a benchmark to assess the adequacy of their reporting. These organizations are refining their programs and looking for clarity on what qualifies as sufficient explanation under the law’s “comply or explain” model.

- Globally Regulated Reporters: These are companies already subject to international mandates such as the EU’s CSRD or the UK’s climate reporting requirements and have been reporting sustainability metrics for many years. For them, the focus is on ensuring their disclosures are harmonized across jurisdictions while meeting SB 261’s expectations—especially as the global climate disclosure landscape rapidly converges.

While CARB has yet to release detailed guidance, they’ve indicated a lenient approach in the first year. That said, we are helping clients take a “no regrets” approach—ensuring their disclosures are comprehensive enough to stand up to future scrutiny, should expectations tighten.

What does “comply or explain” mean?

Under California SB 219, if a company chooses not to fully comply with the TCFD-aligned disclosure requirements, the statute allows for a “comply or explain” approach. This means the company must provide an adequate explanation for any omissions. While CARB has yet to release detailed guidance, they’ve indicated a lenient approach in the first year. That said, we recommend companies attempt to prepare a “no regrets” disclosure to a build defensible disclosure that is comprehensive enough to stand up to future scrutiny, should expectations tighten. A “no regrets” disclosure means when a company does not comply they:

(1) Specify the gap

Be transparent if there is an omission and clearly specify which TCFD elements are not being disclosed (e.g., scenario analysis, metrics and targets).

(2) Provide context

The explanation should describe why the organization is not disclosing the requirement (for example, insufficient internal capabilities, lack of data, or progress underway). The explanation should also provide rationale grounded in the company’s business model, sector, risk exposure, and maturity of its climate risk program. A one-size-fits-all excuse is unlikely to be acceptable.

(3) Provide forward-facing planned actions

An explanation should outline plans to address the gap or improve in the future—ideally with a timeline, even if tentative, and internal subject matter experts involved (if known). This shows a commitment to maturing the program and aligns with the intent of SB 261 to encourage progress over time.

(4) Are consistent with global norms

If the company is following another reporting framework (e.g., CSRD, ISSB, CDP), the explanation should reference this alignment to demonstrate that the disclosure is not lacking rigor, just using a different format or standard.

This kind of thoughtful transparency not only satisfies regulators but builds trust with stakeholders who are increasingly scrutinizing the credibility of climate disclosures.

Looking Ahead: What to Expect and How to Prepare

We anticipate the final SB 219 rule will be released by July 1st. CARB has scheduled a public workshop on May 29th. GSI will be monitoring these discussions closely ensure our clients remain at the forefront of any developments. In the meantime, we will post periodic articles to support reporters as they build or refine their disclosures focusing on:

- Integrating climate-related risk into existing risk management practices

- Understanding the public comments going into the final rule

- Tips for GHG assurance

- The role of climate scenario analysis

- Leveraging existing CDP reporting

- Alignment with other global jurisdictions

- Summaries of the evolving US climate regulatory landscape.

For now, our advice remains consistent: prepare an assurable GHG inventory, disclose progress transparently, and document your rationale thoroughly. This “no regrets” approach means your organization is ready—whether CARB maintains a lenient stance or shifts to a stricter interpretation in future years.

As GSI Environmental’s Principal Scientist and Principal Engineer, we—Becky Twohey and Albert Chung—are excited to support organizations as they prepare for these new requirements and work toward integrating robust climate disclosure practices.

In the next installment, we’ll explore what stakeholders shared in the public comment period leading up to the final rule. Stay tuned for: “What Do Stakeholders Say About CA SB 261 and SB 253? Public Commentary Summarized.” We’ll highlight key themes from public comments submitted to CARB and discuss how this feedback is shaping implementation.

Make sure to follow along as we continue to unpack what these regulations mean for your business, and how you can prepare.

If this information is new to you, or you have questions about how these regulations will affect your business specifically, please feel free to reach out. Our team has decades of combined experience and is able to support all aspects of CA SB 219 compliance.