CARB May Update: New insight provided into California Climate Disclosure roadmap

CARB climate reporting update: On Thursday May 29, the California Air Resources Board (CARB) hosted a workshop covering the major comments it...

CARB climate reporting update: On Thursday May 29, the California Air Resources Board (CARB) hosted a workshop covering the major comments it...

CARB climate reporting update: On Thursday May 29, the California Air Resources Board (CARB) hosted a workshop covering the major comments it received during the informal solicitation period which took place from December 16, 2024 to March 21, 2025. The workshop was highly anticipated with over 3,000 people signed up to attend across five continents.

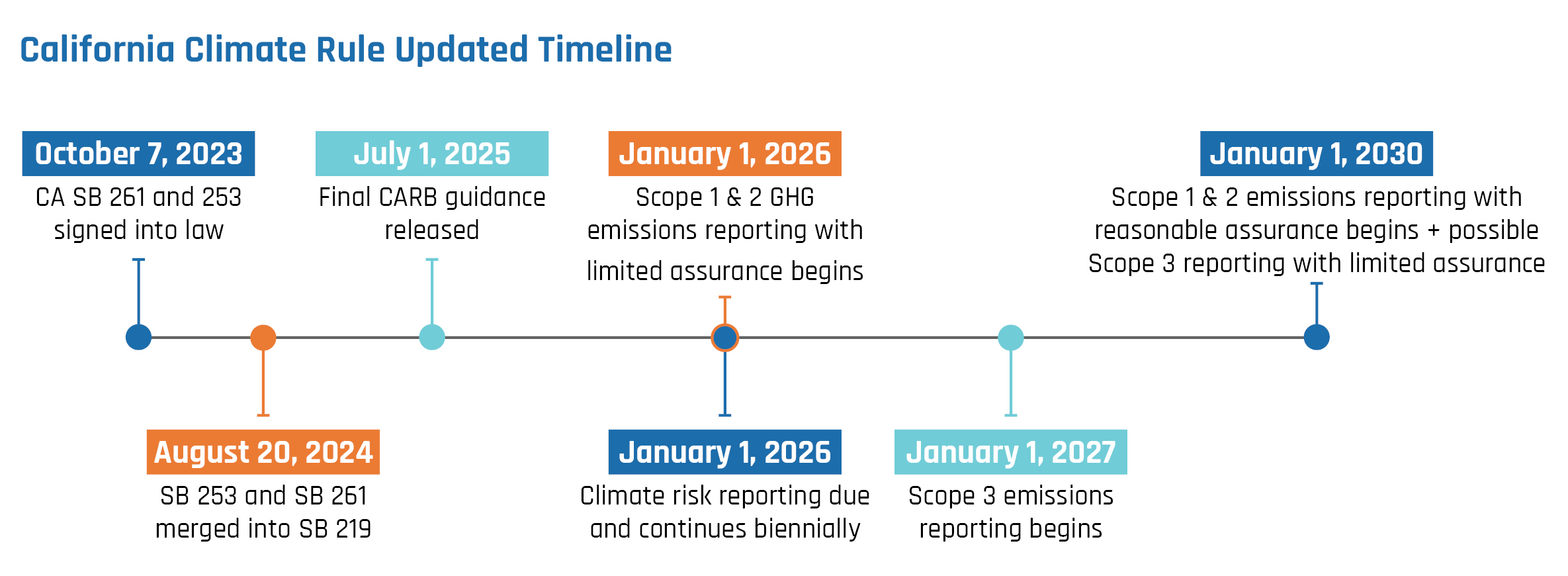

The workshop (where presented information can be found here) was the first significant communication from CARB about the rulemaking status since the enforcement notice that was issued in December 2024. While the presentation provided useful insight into how CARB is thinking about major questions preparers have, it was also clear that much remained to be determined before the quickly approaching 2026 deadline. Below are a few of the major themes that emerged from the workshop.

Throughout the workshop, CARB emphasized that it would rely heavily on comments and key stakeholder input to draft and refine the final rules. As part of the formal rulemaking process, a 45-day comment period will be held once the draft regulatory text is released. The agency is fielding comments and insights at any time through its designated email address, ClimateDisclosure@arb.ca.gov.

CARB reiterated that reporting timelines under SB 253 and SB 261 are fixed. The following deadlines were confirmed:

However, many commenters expressed concern that specific filing dates have not yet been clarified. Given the complexity of developing complete GHG inventories—particularly for companies reporting Scope 3 emissions—there were calls to ensure that deadlines are not set too early in the calendar year.

In addition, while the law calls for limited assurance on 2025 data, CARB has indicated that audit requirements may be deferred until later in 2026, providing preparers with more time to meet assurance expectations.

As companies seek to align with multiple frameworks, stakeholders have requested clarification on how California’s climate risk disclosure requirements (SB 261) will align with global standards, such as the International Sustainability Standards Board (ISSB) and the EU’s Corporate Sustainability Reporting Directive (CSRD). Senators Scott Wiener and Henry Stern—authors of the legislation—confirmed that international alignment remains a top priority and noted ongoing evaluation of standards from Australia, Japan, the UK, and New Zealand as well.

While CARB has tried to allay fears from preparers about a potentially tight reporting timeline by saying that “CARB will exercise enforcement discretion for the first reporting cycle, on the condition that entities demonstrate good faith efforts to comply with the requirements of the law”, several stakeholders—including GSI Principal Becky Twohey—pressed CARB for clarity on what constitutes a “good faith disclosure” under SB 261. While the agency acknowledged the importance of this definition, it has not yet provided further guidance.

The disbanding of the Task Force on Climate-related Financial Disclosures (TCFD) also fueled additional questions, as stakeholders emphasized the need for a clear path forward on which standards companies should use when preparing their disclosures. There remain open questions about whether there are disclosures that are optional in TCFD or IFRS that will become mandatory under SB261.

CARB is currently exploring whether to use California’s Revenue and Taxation Code to define what constitutes “doing business in California”—a key determinant of which companies are subject to the new disclosure rules. However, stakeholders raised concerns about this approach. One recurring theme was the risk of unintended consequences, such as companies choosing not to hire remote workers in California to avoid triggering disclosure obligations. Additionally, there was skepticism about the relationship between having “business in California” and producing emissions in the state.

This uncertainty underscores the urgency for clear guidance, especially as CARB prepares to issue an updated draft rule by July 1, 2025, as required under SB 219. Reporting entities are actively watching for these updates, hoping for clarification on scope, timing, and implementation strategy.

GSI Environmental fully supports CARB’s efforts to bring standardized, transparent climate disclosure to California. We recognize the magnitude of the challenge ahead and the complexity of harmonizing state mandates with international expectations. While we look forward to reviewing the forthcoming draft rules, we also anticipate that delays or clarifications may be necessary to ensure feasible and effective implementation.

As we move forward, we remain committed to partnering with CARB, our clients, and fellow stakeholders to advance climate resilience, data quality, and regulatory preparedness across all sectors operating in California.

In the context of Senate Bills 261 and 253, amended to SB 219, The California Air Resource Board (CARB) has been designated...

In the context of Senate Bills 261 and 253, amended to SB 219, The California Air Resource Board (CARB) has been designated as the regulatory and enforcement authority:

CARB is the state agency responsible for protecting public health by reducing air pollution and overseeing climate policy implementation in California. As part of its broader mandate, CARB plays a key role in advancing the state’s climate goals and ensuring compliance with greenhouse gas (GHG) emissions regulations.

CARB is currently in the process of developing guidance, timelines, and reporting standards for both bills, with public workshops and stakeholder engagement to inform the final rulemaking process. Their goal is to ensure consistent, transparent, and actionable climate disclosures from companies operating in California.

During the regulatory comment period, stakeholders submitted a wide range of feedback, reflecting diverse perspectives from industry, advocacy groups, and the public. GSI Environmental’s sustainability team has summarized and outlined seven major themes of the public comments submitted to CARB.

1. Clarifying Definitions and Scope

Many commenters expressed support for adopting standardized and existing definitions to reduce ambiguity. For example, there was broad endorsement of using California Revenue & Tax Code §23101 to define “doing business in California,” a critical threshold for determining which companies are subject to the disclosure requirements. Currently, CA SB 219 applies to companies that meet the revenue thresholds established in SB 253 (applies to companies with total annual revenues exceeding $1 billion) and SB 261 (applies to companies with total annual revenues exceeding $500 million). Under the California Revenue & Tax Code §23101, a company is considered to be “doing business” in California if it meets any of the following criteria:

Additionally, stakeholders sought explicit clarification on exemptions. Suggestions included specifying whether entities such as government agencies or out-of-state firms with minimal California market presence are subject to the rules. This clarity is essential for consistent application and enforcement.

2. Avoiding Duplication and Minimizing Compliance Burdens

Businesses and industry groups urged regulators to avoid duplicative reporting requirements, emphasizing the need to leverage existing disclosures already made to the U.S. Securities and Exchange Commission (SEC) or under international standards like the Taskforce on Climate-Related Financial Disclosures (TCFD), or International Sustainability Standards Board (ISSB).

Particular concern was raised around the cost-effectiveness of reporting Scope 3 emissions, which require collecting data from across a company’s value chain. CWhile Scope 3 remains the most difficult to decarbonize for the majority of companies, it has been instrumental in driving improvement on the supply-side of the equation by signaling the scrutiny and appetite on the demand-side for green solutions. With the SEC initially dropping Scope 3 reporting requirements, only to eventually drop the climate rule altogether, all eyes are now on CARB to set the bar.

3. Alignment with Existing Global Standards

Similarly, a clear theme across the comments was the importance of aligning California’s disclosure rules with widely recognized international standards such as:

Commenters emphasized that alignment would minimize the compliance burden for multinational companies and ensure that California’s framework is interoperable with emerging global regimes, such as those in Canada, Australia, Europe, Taiwan, Japan, Brazil, etc.

4. Phased and Practical Implementation

Many businesses and assurance providers requested a phased approach, particularly for complex reporting requirements like Scope 3 emissions. Commenters highlighted that third-party assurance markets are not yet fully equipped to handle large-scale Scope 3 verification and called for realistic timelines that recognize current data limitations and resource constraints.

Phased implementation would allow companies to build internal capabilities and data infrastructure over time.

5. Third-Party Reporting and Data Standardization

There was strong support for leveraging third-party platforms such as the CDP (formerly the Carbon Disclosure Project) and The Climate Registry to streamline reporting and reduce duplication.

In addition, stakeholders advocated for the use of machine-readable, standardized formats such as XBRL (eXtensible Business Reporting Language) to facilitate data access, analysis, and public transparency (same as is required by EU in the Corporate Sustainability Reporting Directive).

6. Flexibility Versus Consistency in Reporting

Not surprisingly, opinions diverged on the need for flexibility versus consistency. Environmental advocates stressed the importance of standardized reporting to allow for comparison across companies and sectors. Meanwhile, technology firms and other stakeholders pushed for a more flexible approach that could accommodate evolving methodologies, data tools, and industry-specific nuances.

Finding the right balance between rigor and adaptability remains a key challenge for regulators.

7. Environmental Justice and Public Transparency

Public commenters and environmental justice organizations emphasized the societal value of transparency and the equitable distribution of climate mitigation benefits. They urged CARB to ensure that climate disclosures are publicly accessible and framed in a way that empowers affected communities.

There were also calls to integrate environmental justice considerations into risk disclosures to highlight how climate impacts disproportionately affect low-income and marginalized communities.

California’s climate disclosure legislation—SB 253, SB 261, and the clarifying amendments in SB 219—sets a new precedent for corporate transparency and accountability in the United States. As companies begin preparing for implementation, understanding the regulatory landscape and stakeholder perspectives is an essential first step.

In the next article, we will turn our attention to how companies can leverage their existing risk management practices to both comply and create value: “III. Integrating Climate into Existing Risk Management.” We’ll explore how both COSO Enterprise Risk Management (ERM) and ISO 31000 offer well-established, recognizable and credible processes to build on, and the synergies between existing risk management principles and climate-related financial risk reporting.

Disclaimer: This blog is for informational purposes only and does not constitute legal or compliance advice. Companies should consult with legal counsel and relevant experts to determine specific obligations and develop a tailored compliance strategy.

Sources for all articles:

California State Legislature. Senate Bill No. 253: Climate Corporate Data Accountability Act. 2023. https://leginfo.legislature.ca.gov/faces/billNavClient.xhtml?bill_id=202320240SB253. Accessed 31 Mar. 2025.

California State Legislature. Senate Bill No. 261: Climate-Related Financial Risk Disclosure Act. 2023. https://leginfo.legislature.ca.gov/faces/billNavClient.xhtml?bill_id=202320240SB261. Accessed 31 Mar. 2025.

California State Legislature. Senate Bill No. 219: Climate Accountability Implementation Act. 2024. https://leginfo.legislature.ca.gov/faces/billNavClient.xhtml?bill_id=202320240SB219. Accessed 31 Mar. 2025.

California Air Resources Board. Approved Comments: Climate Corporate Data Accountability Act (SB 253) and Climate-Related Financial Risk Disclosure (SB 261). California Environmental Protection Agency, https://ww2.arb.ca.gov/approved-comments?entity_id=41096. Accessed 31 Mar. 2025.

United States Securities and Exchange Commission. Press Release: SEC Adopts Rules to Enhance and Standardize Climate-Related Disclosures for Investors. United States Securities and Exchange Commission, https://www.sec.gov/newsroom/press-releases/2024-31. Accessed 21 May. 2025

SB 219 Compliance California California has long been at the forefront of national environmental and climate policy, setting ambitious goals for reducing...

California has long been at the forefront of national environmental and climate policy, setting ambitious goals for reducing GHG emissions and promoting sustainable initiatives. With the passage of Senate Bills 253 and 261, further amended by Senate Bill 219, the state is implementing one of the most significant climate disclosure frameworks in the United States. These laws, scheduled to be in effect January 1, 2026, require thousands of public and private companies to disclose detailed information about their greenhouse gas (GHG) emissions and climate-related financial risks. For companies that do business in California, understanding the implications of this legislation is critical for compliance, risk management, and long-term planning.

This is the first of a multi-part series of articles that GSI will publish over the next several months. The series will provide an overview of the California climate legislation, highlight key concerns and recommendations raised during the public comment process, and offer guidance on how businesses can prepare for successful implementation. We will also take a global look at how California climate disclosures align with those in other jurisdictions and give our thoughts on the process of Climate Risk Assessments and Climate Scenario Analysis. We will wrap up the series after the California Air Resource Board (CARB) releases the final rule.

We will start this series by discussing what these bills hope to accomplish, and their basic requirements.

Overview of Senate Bills 253 and 261, as Amended by SB 219

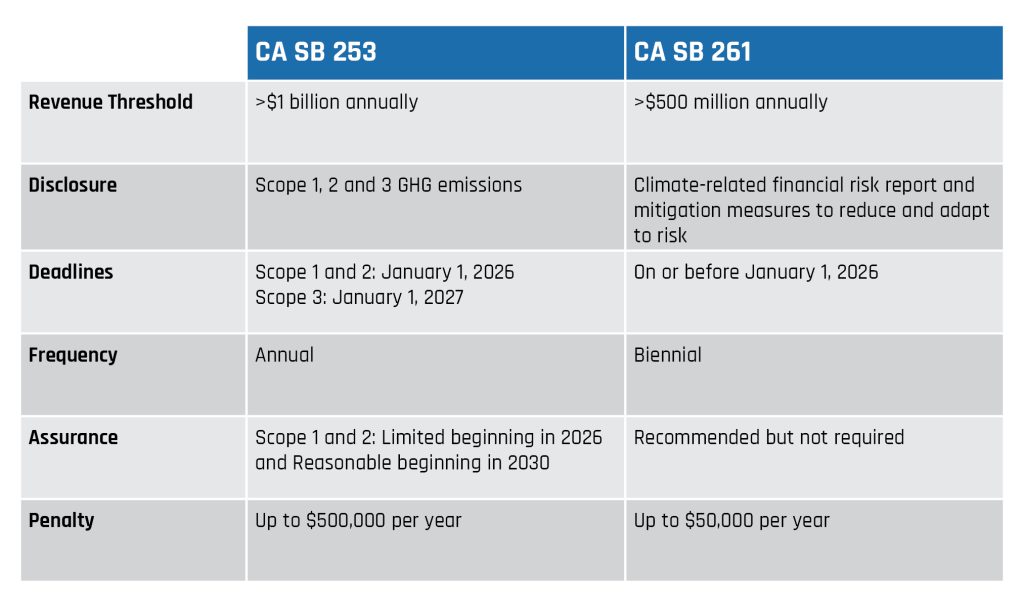

Senate Bill 253 (SB 253): Known as the Climate Corporate Data Accountability Act, SB 253 requires companies with annual revenues over $1 billion and doing business in California to publicly disclose their full GHG emissions, including Scope 1 (direct emissions), Scope 2 (indirect emissions from purchased electricity), and Scope 3 (all other indirect emissions in a company’s value chain). Reporting must be conducted in accordance with the Greenhouse Gas Protocol and initially subject to third-party limited assurance. The required assurance level for Scope 1 and Scope 2 emissions disclosures potentially increases to a reasonable assurance level in 2030.

Senate Bill 261 (SB 261): Referred to as the Climate-Related Financial Risk Disclosure Act, this bill mandates that companies with annual revenues over $500 million doing business in California prepare biennial reports detailing their climate-related financial risks and the strategies they employ to mitigate these risks. These disclosures must align with the Task Force on Climate-related Financial Disclosures (TCFD) framework.

Senate Bill 219 (SB 219): SB 219 amends SB 253 and SB 261 to address implementation challenges and better incorporation of stakeholder feedback. Notable amendments include clarifications on compliance timelines, improved alignment with federal and international standards, and greater specificity around agency responsibilities and data reporting formats. Of most interest to reporting companies is that:

Evaluating your current readiness

These bills position California as a national leader in climate transparency and put significant obligations on a wide swath of companies operating in or connected to the state. As California’s SB 219 disclosure requirements move closer towards implementation, companies subject to the law are navigating an evolving landscape—often without clear regulatory guidance. At GSI, we’ve been working closely with clients across sectors to prepare robust, defensible disclosures, grounded in best practices and aligned with international standards. We also have extensive experience in CARB rulemaking for various regulations including AB32 (Global Warming Solutions Act of 2006). From our experience with CARB and sustainability reporting, CA SB 219 reporters generally fall into three categories:

While CARB has yet to release detailed guidance, they’ve indicated a lenient approach in the first year. That said, we are helping clients take a “no regrets” approach—ensuring their disclosures are comprehensive enough to stand up to future scrutiny, should expectations tighten.

What does “comply or explain” mean?

Under California SB 219, if a company chooses not to fully comply with the TCFD-aligned disclosure requirements, the statute allows for a “comply or explain” approach. This means the company must provide an adequate explanation for any omissions. While CARB has yet to release detailed guidance, they’ve indicated a lenient approach in the first year. That said, we recommend companies attempt to prepare a “no regrets” disclosure to a build defensible disclosure that is comprehensive enough to stand up to future scrutiny, should expectations tighten. A “no regrets” disclosure means when a company does not comply they:

(1) Specify the gap

Be transparent if there is an omission and clearly specify which TCFD elements are not being disclosed (e.g., scenario analysis, metrics and targets).

(2) Provide context

The explanation should describe why the organization is not disclosing the requirement (for example, insufficient internal capabilities, lack of data, or progress underway). The explanation should also provide rationale grounded in the company’s business model, sector, risk exposure, and maturity of its climate risk program. A one-size-fits-all excuse is unlikely to be acceptable.

(3) Provide forward-facing planned actions

An explanation should outline plans to address the gap or improve in the future—ideally with a timeline, even if tentative, and internal subject matter experts involved (if known). This shows a commitment to maturing the program and aligns with the intent of SB 261 to encourage progress over time.

(4) Are consistent with global norms

If the company is following another reporting framework (e.g., CSRD, ISSB, CDP), the explanation should reference this alignment to demonstrate that the disclosure is not lacking rigor, just using a different format or standard.

This kind of thoughtful transparency not only satisfies regulators but builds trust with stakeholders who are increasingly scrutinizing the credibility of climate disclosures.

Looking Ahead: What to Expect and How to Prepare

We anticipate the final SB 219 rule will be released by July 1st. CARB has scheduled a public workshop on May 29th. GSI will be monitoring these discussions closely ensure our clients remain at the forefront of any developments. In the meantime, we will post periodic articles to support reporters as they build or refine their disclosures focusing on:

For now, our advice remains consistent: prepare an assurable GHG inventory, disclose progress transparently, and document your rationale thoroughly. This “no regrets” approach means your organization is ready—whether CARB maintains a lenient stance or shifts to a stricter interpretation in future years.

As GSI Environmental’s Principal Scientist and Principal Engineer, we—Becky Twohey and Albert Chung—are excited to support organizations as they prepare for these new requirements and work toward integrating robust climate disclosure practices.

In the next installment, we’ll explore what stakeholders shared in the public comment period leading up to the final rule. Stay tuned for: “What Do Stakeholders Say About CA SB 261 and SB 253? Public Commentary Summarized.” We’ll highlight key themes from public comments submitted to CARB and discuss how this feedback is shaping implementation.

Make sure to follow along as we continue to unpack what these regulations mean for your business, and how you can prepare.

If this information is new to you, or you have questions about how these regulations will affect your business specifically, please feel free to reach out. Our team has decades of combined experience and is able to support all aspects of CA SB 219 compliance.

Greenhouse gas (GHG) verification – the independent review of your emissions data – is becoming an expected step in sustainability reporting. Sustainability...

Greenhouse gas (GHG) verification – the independent review of your emissions data – is becoming an expected step in sustainability reporting. Sustainability information is becoming more vital to stakeholder decision-making. Voluntary frameworks and regulators alike are increasingly emphasizing the importance of verified disclosures. For example, CDP encourages companies to verify their emissions (offering scoring boosts for third-party assured data) and upcoming regulations require verification such as California’s SB 253 and SB 261, Europe’s Corporate Sustainability Reporting Directive (CSRD), and more. The trend is clear: whether for investors, customers, or compliance, your sustainability data needs to be accurate, reliable, and easy to verify.

As assurance, specifically GHG Verification, becomes more common, many preparers wonder how to ensure a successful audit and confidence in their disclosures. Here are some steps that companies can take in the short, medium, and long term to ensure satisfied stakeholders (and verifiers).

First, a note: A recurring theme from industry leaders is that sustainability information should be as trustworthy as financial statements. Based on current trends, it would not be surprising if carbon data will soon appear alongside financial results if they are not already. As a result, this data must be prepared with the same level of precision and quality control. As a GHG inventory preparer, you should gear your process to satisfy a reasonable assurance audit even if you’re only undergoing limited assurance now. Building early robust practices will prepare you as stakeholders demand deeper scrutiny of emissions data.

Short-Term: Strong internal controls and checks

Implementing internal quality controls on your data is one of the most important steps to improve verifiability. In practice, this involves establishing procedures to ensure accuracy, completeness, and consistency at every stage of inventory preparation. The Greenhouse Gas Protocol outlines some examples of simple controls to have in place quickly, including:

To streamline the process, leverage your organization’s expertise in financial controls—for example, involve internal audit or IT teams to help set up data controls.

Medium Term: Inventory Management Plans

Once the core components of a process are in place, the next step is to formalize them as part of an Inventory Management Plan (IMP). An IMP is a living manual for your inventory process. Per the EPA, it “describes an organization’s process for completing a high-quality, corporate-wide GHG inventory.”

In practical terms, an IMP documents all the key aspects of your GHG accounting program, including:

By formalizing the process in an IMP, preparers ensure consistency year after year. The key is that an IMP is not a static document; it should evolve with your company. Investing time in a thorough IMP makes annual reporting more routine and verification-ready. Importantly, companies with well-thought-out IMP often find that third-party auditors have an easier job and ask fewer remedial questions because all the information on processes and methods is readily available and organized.

Long-Term: Continuous improvement

In the long run, the goal is to bake quality and verification-readiness into the DNA of your carbon management. Treat each verification cycle not just as a test to pass but as an opportunity to learn and improve. Verification findings often come with recommendations for better data or controls; the GHG Protocol suggests viewing the process “as a valuable input to the process of continual improvement.”

For instance, if your verifier notes a weakness – say, inconsistent record-keeping at one facility – use that insight to strengthen your system before the next cycle. Over years, these incremental upgrades lead to a very robust inventory process. In the long term, companies should aim to integrate GHG data management into their broader governance frameworks. Sustainability data should not live in a silo. Many leading companies are now aligning their carbon data management with financial reporting systems – some even map it to internal control frameworks like SOX. The rationale is that carbon emissions involve financial implications (energy cost, carbon pricing, etc.), so managing this data with the same rigor is just good business practice.

Similarly, long-term planning includes keeping an eye on evolving standards. New protocols, updated GHG calculation guidance, or new regulatory criteria may emerge (for example, the GHG Protocol’s Standards are being updated at this time). Ensuring your team stays educated – perhaps through training or participation in industry groups – will help future-proof your inventory.

Lastly, consider broadening the scope of what you verify over time. Many organizations start with getting limited assurance on their Scope 1 and 2 emissions. They may extend verification to Scope 3 emissions as they mature or move to reasonable assurance for a comprehensive data audit. This phased approach is sensible: it allows you to build confidence and systems gradually. However, the end-state vision is clear: a fully transparent, credible GHG inventory process that stakeholders can trust, year after year, as much as they trust the financial books. Achieving that level of reliability is a journey that starts with the concrete steps outlined above.

In conclusion, passing a GHG verification (whether a limited review or a rigorous reasonable assurance engagement) comes down to preparation and good data practices. By implementing internal controls, documenting your methods in an inventory management plan, and using reputable data sources, you make an auditor’s job straightforward and greatly increase the credibility of your climate reporting. As verification requirements ramp up across voluntary programs and mandatory regulations, organizations that proactively strengthen their GHG inventories will find the process far less daunting. Beyond just “passing” verification, you’ll provide the kind of trusted information investors and other stakeholders are increasingly looking for. If you need Greenhouse gas (GHG) verification, we can help.