Why CA SB 343 Demands Immediate Attention

From California SB 343, to Colorado’s HB 2201355, to the EU Green Claims Directive, regulators around the world are cracking down on...

From California SB 343, to Colorado’s HB 2201355, to the EU Green Claims Directive, regulators around the world are cracking down on...

From California SB 343, to Colorado’s HB 2201355, to the EU Green Claims Directive, regulators around the world are cracking down on greenwashing regulations and putting companies on notice. The message is clear: If you say our product is recyclable, it better be true.

California Senate Bill 343 is one of the most stringent and enforceable laws regulating environmental marketing claims regarding recyclability of products and packaging materials. With the release of the CA SB 343 Final Findings Report on April 4, 2025, the countdown has begun for companies to bring their packaging and sustainability claims into full compliance by October 4, 2026.

Who Should Pay Attention?

Businesses that create, manufacture, import, or sell consumer goods, including brand owners, retailers, packaging designers, printers, and labelers, should be aware of the important regulations set forth in CA SB 343. If your product or packaging includes any sustainability claims, whether explicit or implied, it’s crucial to ensure compliance with these guidelines. This includes any statements suggesting that your product is eco-friendly or encouraging consumers to recycle or compost. If you’re operating in California and promoting environmentally friendly initiatives while using materials like plastic, glass, metal, ceramic, paper, fiber, wood, or organic substances, it’s essential to take proactive steps to align with these regulations.

The Era of Loose Recycling Claims is Over

CA SB 343 targets greenwashing head-on by establishing strict requirements for organizations that wish to make recyclability claims in their products or packaging. It prohibits the use of the Universal Recycling Symbol (the Mobius Loop) and the placement of resin identification codes within the symbol unless the product or packaging material meets strict statewide criteria for recyclability. The law will remove vague or misleading claims about recyclability, ensuring that only genuine, compliant products can make such claims. CalRecycle is responsible for determining the percentage thresholds for recyclability claims in the current Findings Report and any subsequent reports to follow.

If your label says it is recyclable, it must meet the following thresholds:

If your product does not check all three boxes, calling it recyclable or displaying the Mobius Loop is considered a “deceptive or misleading claim” under California law. Such violations are classified as misdemeanors and are subject to enforcement by the Attorney General, local prosecutors, and private lawsuits under unfair competition laws.

Why Businesses Should Care About Greenwashing Regulations

SB 343 is part of a global regulatory shift toward validated sustainability marketing. Brands that take proactive steps will protect themselves from risk and potentially gain a competitive advantage in a market increasingly shaped by customer trust and regulatory scrutiny.

By October 2026, companies must:

Don’t wait until 2026. Navigating SB 343 compliance is a chance to build resilience and gain customer trust. At GSI, we specialize in helping companies bridge the gap between sustainability goals and regulatory compliance. Our team of scientists, engineers, and environmental experts can map your full packaging inventory against SB 343 standards, assess recyclability and compostability using recognized testing protocols, flag at-risk SKUs, recommend design or material alternatives, and provide documentation and claim substantiation for audits or legal scrutiny. We can also develop tracking methods to ensure outbound products meet the various compliance markets beyond California.

At the heart of climate disclosures is a “climate scenario analysis” or "climate risk scenario planning" which may baffle and frustrate many...

At the heart of climate disclosures is a “climate scenario analysis” or “climate risk scenario planning” which may baffle and frustrate many first-time climate reporters. This article is meant to provide context and make CSAs more accessible. It reflects on our experience working with a wide range of clients across different industries, summarizing the key challenges companies face with climate scenario analysis, the use of qualitative versus quantitative analysis, and how climate scenario analysis fits into a company’s existing processes. Our goal is to not only help companies comply with investor or regulatory CSA requirements, but to add value to their business planning by helping companies understand and anticipate their risk exposure and identify a range of strategic options that you may not be aware of.

How did we get here?

1970s-1980s: Climate scenario analysis began as a forward-looking planning tool used by Shell and then other energy companies to explore oil price volatility and long-term energy trends.

1990s: Climate scientists and economists developed integrated assessment models (IAMs) to link emissions, climate outcomes, and policy responses, forming the basis for IPCC scenarios commonly used in CSAs.

2000s: Financial institutions began recognizing climate change as a systemic risk. Key industries—including energy, finance, agriculture, and manufacturing—began adopting scenario planning to assess exposure to both transition and physical climate risks. Likewise, utilities and municipalities began using climate impact studies to model long-term physical risks like heatwaves, droughts, and infrastructure vulnerability, integrating findings into infrastructure resilience, urban planning and investment planning.

2015 Paris Agreement: The G20’s Financial Stability Board created the Task Force on Climate-related Financial Disclosures (TCFD) which formally recommended climate scenario analysis as part of corporate risk disclosure.

2019: Central banks like the Bank of England and the NGFS began climate stress tests for financial institutions, accelerating adoption.

2022–Present: Climate scenario analysis became a regulatory requirement in major jurisdictions under frameworks like California’s SB 219, the EU’s CSRD, the UK’s TCFD-aligned rules, Canada’s OSFI guidance, and Australia’s IFRS S2-based standards.

Key Challenges for Companies

Across the industries and clients GSI serves, there are challenges that we must overcome both in terms of building trust and capacity with our clients in terms of how they rely on and use the analysis, and that we disclose for liability purposes.

Client data gaps and quality: One of the biggest challenges is the scarcity and/or inconsistency of data. We find limitations in emissions and asset data (especially for supply chains and smaller counterparties) common, as well as gaps in company–specific loss data. Regulators (e.g. NGFS, FSB) report that data deficiencies can understate climate risk and make results unreliable. To overcome these gaps, we often piece together information from public sources or third-party providers, but this increases uncertainty.

Methodological complexity: Climate scenario analysis spans diverse disciplines (climate science, economics, finance), making integration difficult. The Central Bank NGFS guide notes “climate scenarios provide a flexible ‘what-if’ framework,” and linking physical climate outcomes with macroeconomic and financial impacts remains a work in progress. In practice, we may use multiple model types and simplifying assumptions to make the analysis relevant and feasible, but this again increases uncertainty.

Uncertain scenarios: We are in uncharted territory, and the future trajectory of climate change and policy is highly uncertain. We must select a range of plausible scenarios (e.g. below-2°C “orderly transition” versus high-warming “hot house” pathways), but there is no single best set of scenarios. Each scenario’s assumptions (carbon prices, technology uptake, physical effects, etc.) have high uncertainty. In practice, we recommend companies run as many scenarios as makes sense; this judgment is inherently subjective unless determined by reporting jurisdiction.

Internal capabilities and governance: Many companies we work with are still building their climate expertise, where the CSA is led by mid-level managers or a sustainability team with limited access across key functional roles or authority. Because key business units (finance, operations, procurement, strategy) may have little input, the results may be too technical or miss opportunities to make an impact across the company. Without strong governance and board oversight, scenario planning risks remaining an academic or compliance exercise.

Regulatory alignment and “alphabet soup”: Companies must navigate multiple, sometimes overlapping regulations and frameworks. Besides California’s SB 219 (TCFD or IFRS), they may face the EU’s CSRD, UK’s TCFD-aligned mandates, Canada’s OSFI Guideline B-15, Australia’s upcoming IFRS S2-based disclosures, and others. Each has its own nuances (different scope definitions, disclosure formats, scenario specifications). Aligning efforts to satisfy all requirements (e.g. scenario outputs that meet both CSRD/ESRS and IFRS S2, which may differ slightly) adds to the challenge, risking duplication and compliance burden (see our previous article on the topic/link here).

Even as data and models improve, there will always be challenges that we have to disclose.

Integrating Climate Scenarios with Existing Processes

Rather than starting from scratch, we look for ways we can build on established processes:

Risk Management: Scenario analysis should be integrated into the organization’s risk management. If a company has a formalized enterprise risk management framework (ERM), this means treating climate as a key risk category by involving risk officers and audit/ risk committees in overseeing scenario work and ensuring outputs feed into existing risk registers. When ERM teams update risk registers or perform annual risk assessments, they can overlay climate drivers (e.g. carbon-pricing or supply-chain disruptions). (See our previous article on the topic). Similarly, a defined risk appetite makes determining what level of financial, operational, or reputational impact from climate change a company is willing to tolerate. For example, a risk-averse company might stress-test severe scenarios (like a rapid transition to a low-carbon economy) more rigorously than one with a higher risk tolerance.

However, many companies don’t have a formalized ERM, so we can review existing financial disclosures (like a 10K) and engage with key personnel to develop a risk appetite to set the tone for how bold or cautious the company is willing to be when planning for future climate-related events. Even an informal understanding of a company’s risk appetite is useful for a CSA because it influences which climate scenarios are considered. For example, a company with a high appetite for transition risk might embrace scenarios that include rapid policy shifts or technological disruptions. Meanwhile, a company more concerned with physical risks might model chronic climate hazards like rising sea levels or extreme weather.

Operational Risk and Business Continuity: Many companies have robust operational risk management in place already, where climate scenarios are used to further inform risk management and business continuity planning. For example, manufacturing firms can use extreme-weather projections to assess supply-chain risk. Existing operational risk assessments (e.g. scenario plans for factory outages or natural disasters) can be expanded to include climate variables. Firms with physical assets can incorporate long-range climate projections (temperature rise, sea-level) into site plans.

Capital and Strategy Planning: Scenario outputs must be tied back to capital budgeting and business strategy. If a climate scenario implies reduced demand for fossil fuels or stranded assets, investment plans and transition strategies need adjustment. Thus, finance and strategy teams can fold climate-driven revenue/cost projections into their multi-year plans. For example, if an electric utilities company uses a below-2°C scenario, it might factor a faster decline in coal plant revenues into its capital allocation decisions. Integrating climate scenarios into traditional budgeting cycles and strategy reviews ensures the analysis informs real decisions rather than being an isolated report.

By reusing existing frameworks—ERM, stress tests, budget models—companies can make climate scenario planning a practical extension of what they already do. By integrating scenario analysis into strategic planning or risk management, companies can evaluate their strategy. Importantly, this mindset avoids treating CSAs as a compliance, one-off exercise, embedding it into your governance and decision-making.

Modeling Approaches: Qualitative vs. Quantitative

Climate scenario analysis ranges from high-level qualitative narratives to detailed quantitative modeling. TCFD recommends companies start with a qualitative analysis, and we generally agree, and IFRS S2 acknowledges that scenario inputs can be qualitative or quantitative. A smaller company with limited capacity or data might rely primarily on narrative scenarios for several years.

Qualitative narratives: Many companies begin by outlining storylines (e.g. “Net-Zero 2050,” “Delayed Transition,” “Hothouse World”) that describe plausible futures for policy, technology and market conditions. These narratives may note key drivers (carbon price path, energy mix, regulatory changes) without assigning exact values. Such qualitative scenarios help identify broad risk themes and strategic implications. For example, a company might describe a 1.5°C scenario where strict carbon policies accelerate electrification, and another 3°C scenario where action is delayed.

Quantitative modeling: More mature analyses incorporate numeric projections of climate and economic variables. Core tools include:

Hybrid approaches: Most of our corporate scenarios analyses blend narrative and numbers. A firm might start with a published scenario (“2°C gradual transition” or “Delayed action leading to 4°C warming”) and then apply internal financial assumptions. For example, the company’s finance team could take the NGFS 1.5°C pathway for carbon prices and feed it into the enterprise resource planning system to project energy costs and profit margins.

It is critical that we meet our clients where they are in terms of readiness to complete the analysis and organizational capacity to leverage the analysis. Regardless of approach, users of the analysis (including regulatory mandates) require we meticulously document the methodology and under assumptions.

CSA in Action

When done well, a CSA is more than a compliance exercise and can inform decision-making. John Deere, a global leader in agricultural machinery and technology, is exposed to climate-related risks in multiple ways—through its supply chains, customer base (farmers), and resource availability (like water and soil health). Recognizing this, John Deere has started aligning its strategy with climate resilience, using tools like scenario analysis in accordance with TCFD. In its Sustainability Reports and CDP Climate Change responses, John Deere discusses using their existing enterprise risk management criteria in their climate scenario planning to evaluate future risks and opportunities under various temperature rise scenarios (low emissions/RCP 2.6 and high emissions/RCP 8.5). John Deere evaluates how different climate futures could affect agricultural productivity (e.g., how droughts or floods might shift crop production areas), customer behavior (e.g., increased demand for precision agriculture solutions that reduce water and fuel use), supply chain resilience (e.g., disruptions from extreme weather events) and regulatory shifts (e.g., carbon pricing or emissions standards). Their CSA reveals a balanced picture of future climate-related challenges and opportunities:

Physical risks under high emissions futures:

Transitional risks under low emissions futures:

The CSA results have companywide implications to mitigate risk and capitalize on revenue generating opportunities. Their response includes anticipating supply chain disruptions and preparing alternative logistics and sourcing strategies, including scaling renewable energy options by 20%, and investing roughly 2.2B in green innovation such as precision agriculture to reduce inputs and increase yields, electric and hybrid machinery to lower emissions, and digital platforms that help farmers adapt to weather variability and long-term climate trends.

Summary

In summary, climate risk scenario planning spans a spectrum. At one end are qualitative “what-if” narratives; at the other end are fully quantitative simulations that output numeric changes in revenues, costs or asset values. Major climate scenarios and models (RCP/SSP pathways, IEA scenarios, NGFS scenarios) serve as common starting points. We then work with companies to tailor these using the models and data relevant to their industry and geography. Firms with higher climate exposure and capability are expected to use more sophisticated (quantitative) approaches. As internal expertise and the climate field grows, businesses are moving from narrative sketches toward more data-driven scenario projections, while still acknowledging inherent uncertainties.

At GSI, we have worked across this spectrum with a wide range of clients. We have a deep bench of climate modelers and experts. If you have questions or need support, please get in touch with us.

Global momentum of Climate Disclosures While some of our clients are new to climate reporting, it is important to understand that California...

Global momentum of Climate Disclosures

While some of our clients are new to climate reporting, it is important to understand that California climate disclosure laws are not happening in a vacuum – that they align with most other developed economies and regulators. Most sustainability-related disclosure mandates have considerable overlap, meaning that alignment with one regulation often results in alignment or partial alignment with another one. Understanding the key similarities and differences in these reporting standards will help organizations improve their reporting efficiency and meet stakeholder and regulatory demands. Ultimately, the goal is to streamline compliance-based reporting so that companies can focus on strategy and value creation.

How does CA SB 219 compare to other global climate mandates?

CA SB 219 is part of the California Climate Accountability Package, which includes SB 253 and SB 261 – which were amended by SB 219. CA SB 219 requires companies to disclose using the Notably, TCFD was disbanded in 2023 and its functions were fully incorporated into the International Sustainability Standards Board (ISSB) who then drafted IFRS S1 – General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 – Climate-related Disclosures (thus standardizing what was previously guidance in TCFD). IFRS S2 effectively replaces and builds upon the TCFD recommendations.

IFRS S2 brings structure to global climate-related financial risk reporting. The ISSB sustainability reporting requirements have since been enacted by several countries including Australia, Costa Rica, Malaysia, Sri Lanka, Tanzania, Pakistan, and others. Additional jurisdictions such as Canada, China, and Mexico are planning to implement ISSB reporting requirements in the near future (Fig. 1).

Figure 1. The latest IFRS Report shows that more than 30 jurisdictions (together accounting for 57% of global GDP, over 40% of market capitalization, and more than half of worldwide greenhouse gas emissions) have either finalized their plans to adopt ISSB Standards or are actively moving toward their use.

During Senator Weiner reiterated the Senate Bill would align with other global reporting mandates and standards, however he did not state explicitly that IFRS S2 would be a satisfactory reporting standard.

How does TCFD compare to IFRS S1 and S2 Disclosure Requirements?

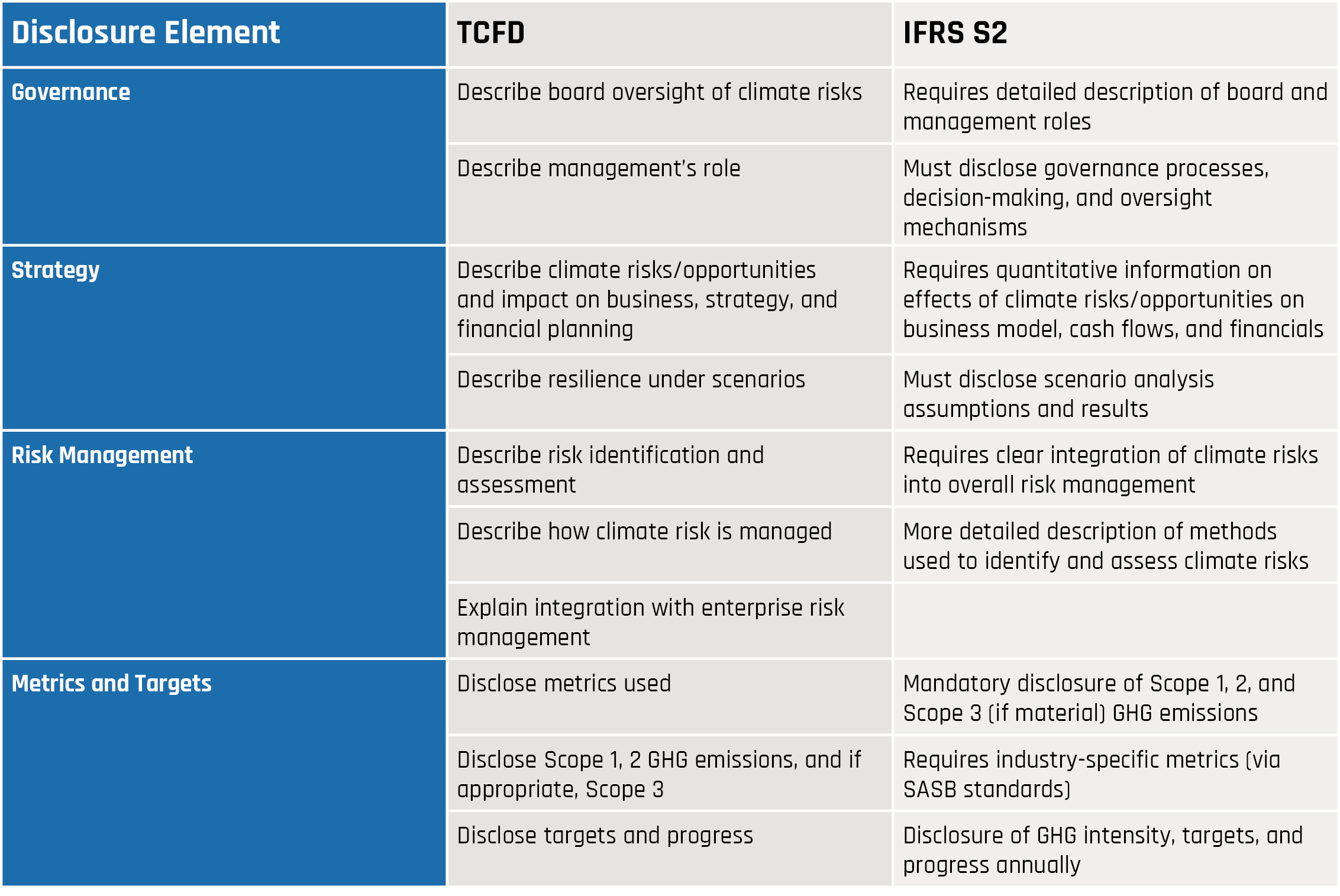

Both the ISSB sustainability standards and TCFD require companies to disclose climate-related financial impacts from a financial materiality perspective, which examines how climate-related risks and opportunities impact a company’s financial performance (such as revenues, cash flows and asset valuations). The disclosure requirements in IFRS S2 significantly build upon the framework established by TCFD, with increasing attention and detail on financial materiality (Table 1).

Table 1. Comparison of disclosure requirements in TCFD and IFRS S2.

In particular, IFRS S2 requires more detailed descriptions of the process for identifying and assessing climate related risks, emphasizing the importance of conducting a climate scenario analysis (CSA).

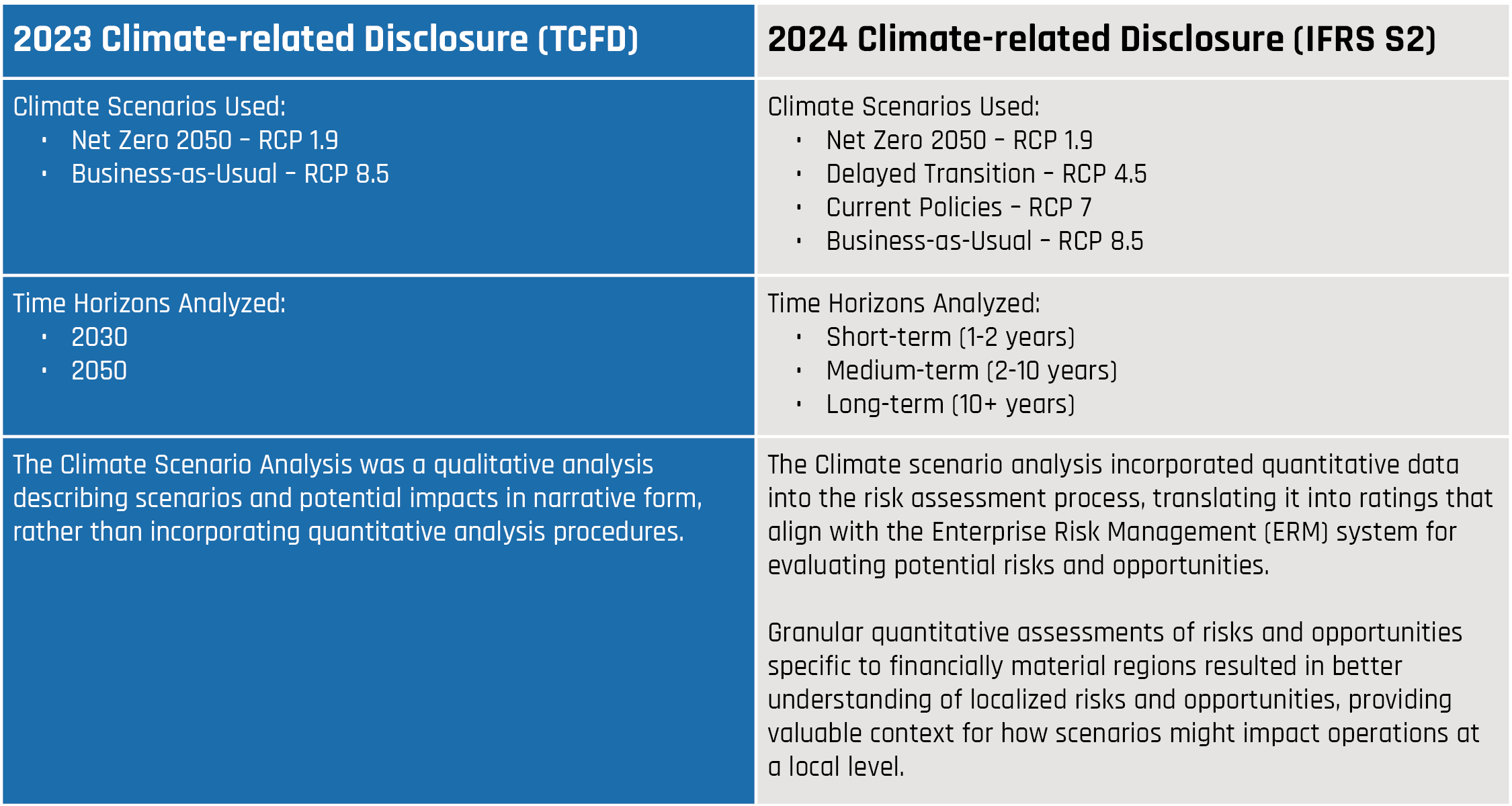

Companies are adjusting their reporting to the changes from TCFD to IFRS accordingly. GSI analyzed public disclosures and found particularly useful examples of the shift from TCFD to IFRS with Wheaton Precious Metals, a Canadian precious metals corporation that primarily sells gold and silver in North America, Europe, Africa, and South America. Wheaton voluntarily reported climate-related disclosures aligned to TCFD in 2022 and 2023. In 2024, Wheaton Precious Metals began reporting their climate-related disclosures aligned to IFRS S2 requirements to meet Canada’s Canadian Sustainability Disclosure Standards (CSDS 1 & CSDS 2) regulatory requirements. The 2024 climate-related disclosures reported to the IFRS S2 significantly build on Wheaton Precious Metals’ previous TCFD disclosures (Table 2).

Table 2. Major differences between Wheaton Precious Metals TCFD-aligned climate-related disclosure from 2023 and their IFR S2-aligned disclosure from 2024.

2023 Climate-related Disclosure (TCFD)

2024 Climate-related Disclosure (IFRS S2)

How does CA SB 219 compare to the EU’s CSRD?

Both California’s Senate Bill 219 and the European Union’s Corporate Sustainability Reporting Directive (CSRD) are key pieces of legislative packages aimed at improving corporate transparency, consistency and quality of climate-related risks and impacts. They are designed to inform investors, regulators and the public about how companies affect and are affected by the environment and social factors. While both CA SB 219 and CSRD align or build upon global reporting standards (TCFD and the GHG Protocol), there are a few key differences.

Differences in Focus Area: CA SB 219 requires companies to disclose climate-related matters only, whereas the European Sustainability Reporting Standards (ESRS) developed for CSRD compliance cover a broad range of environmental, social and governance matters.

It is worth noting that CSRD fully incorporates IFRS S2 disclosure requirements for climate-related disclosures, meaning that companies disclosing CSRD’s climate standard will meet California’s disclosure requirements.

Differences in the Definition of Materiality: CA SB 219 only requires organizations to consider materiality from a financial perspective. Under CA SB 219, all in-scope entities are required to report on Scope 1, 2, and 3 emissions, regardless of materiality. CSRD on the other hand, requires organizations to complete a double materiality assessment (evaluating both impact and financial materiality) and disclose set of ‘General Disclosures’ that cover key sustainability reporting aspects such as governance frameworks, strategy disclosures, and impact management.

In addition, CSRD requires more detailed climate-related information if it is deemed to be material such as metrics on energy consumption, mix, and intensity.

Differences in Scope: CA SB 219 mandates that US-based companies operating in California disclose certain sustainability information. Companies with annual revenues of $1 billion or more must publicly disclose their Scope 1 and Scope 2 emissions starting in 2026, followed by Scope 3 emissions in 2027. Additionally, companies with annual revenues exceeding $500 million are required to disclose climate-related financial risk reports beginning in 2026 with biannual updates.

The EU’s CSRD requires EU-based companies with 250+ employees and at least €50 million in net turnover or a balance sheet exceeding €25 million to disclose sustainability information using applicable ESRS standards. Non-EU-based companies that generate €150 million in net turnover annually within EU member states are also subject to CSRD reporting.

Differences in Disclosure: CA SB 219 requires a greenhouse gas inventory for Scope 1, 2 and ultimately Scope 3 emissions, as well as an aligned Climate-Related Financial Risk Report. CSRD requires detailed disclosures using the European Sustainability Reporting Standards (ESRS), which are aligned with TCFD, as well as GRI and SASB/ISSB IFRS S2.

Differences in Third-party Assurance: CA SB 219 requires limited assurance for Scope 1 and 2 emissions data beginning in 2026 with requirements for reasonable assurance beginning in 2030. Scope 3 emissions data will need limited assurance starting in 2027. There is no escalation of the assurance to reasonable assurance for Scope 3 emissions under CA SB 253. Additionally, there are no third-party assurance requirements for TCFD-aligned climate-related disclosures under CA SB 261.

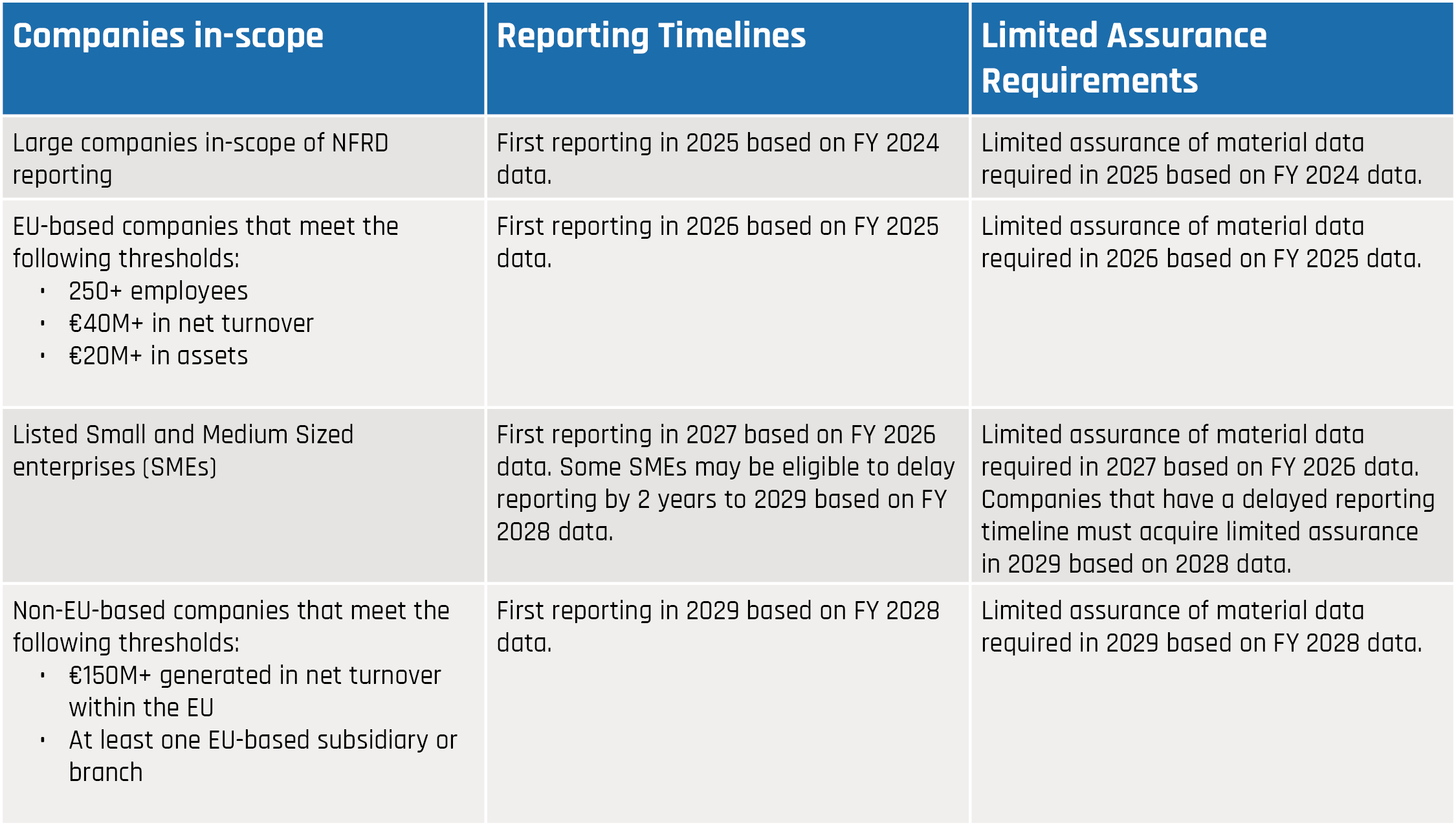

Under CSRD, limited assurance verification procedures are being introduced gradually, aligning to the timelines that correspond to the phased-in implementation for in-scope reporting companies (Table 3). Data assurance is required for all sustainability topics (environmental, social, governance) that have been deemed material through the Double Materiality Process. The European Commission is currently determining if it is feasible to require companies to transition to obtaining reasonable assurance for their sustainability data. The Commission is expected to assess the feasibility of reasonable assurance and adopt corresponding standards no later than October 2028.

Table 3. Phased-in reporting timelines for CSRD data as well as the limited assurance requirement timelines for companies in scope of CSRD reporting.

Differences in Enforcement: CA SB 219 will be enforced by the California Air Resources Board (CARB). In 2024, CARB announced that they will not administer penalties for incomplete Scope 1 and Scope 2 data reported in 2026 as they do not expect all in-scope companies to be fully compliant with the regulations in the first year of reporting. Under CA SB 219, penalties for non-compliance with GHG emission requirements can result in fines of up to $500,000 per reporting year. CARB is expected to adopt final regulations and detail how they will enforce the legislation by July 1, 2025.

Enforcement of CSRD and penalties for non-compliance are handled at the member-state level. Each EU member-state is responsible for translating the CSRD into their national legislature and for ensuring compliance by in-scope entities. Member states can adjust the legislature to fit the needs of their individual country. Although penalties differ by country, non-compliance may lead to fines and penalty fees, legal actions against the company such as audits, investigations, and lawsuits, reputational harm, and in France, potentially even imprisonment for company directors if the non-compliance is considered severe enough.

What are other jurisdictions doing?

As mentioned above, there are over 35 other jurisdictions with proposed or enacted climate reporting mandates. The ISSB standards have been modified in the jurisdictions where they were adopted to reflect local data collection and aggregation methodologies, provide companies with phased-in adoption timelines if necessary, and customize reporting requirements to governmental agencies established standards.

United Kingdom

While the United Kingdom has plans to implement ISSB standards starting in 2026, there are already mandatory sustainability standards in place, namely, the United Kingdom Sustainability Reporting Standards (SRS). These standards are based on the ISSB IFRS S1 and S2 frameworks but have not yet been fully implemented. To facilitate a smoother transition for companies in adopting the full IFRS S1 and S2 standards, organizations subject to the SRS have been mandated to publish TCFD disclosures annually starting in 2022. The range of companies in scope of SRS mandates is narrower than the requirements set by standards such as CA SB 219 and CSRD. The UK SRS is only applicable to companies listed on the United Kingdom Stock Exchange. The scope of companies subject to SRS reporting may increase to include SMEs and privately held firms in the future.

New Zealand

New Zealand developed their own climate-related disclosure standards called the Climate-Related Disclosures Regime in 2023 with the help of the External Reporting Board. Climate disclosures are a key legislative piece of the Financial Sector Climate-related Disclosures act which requires certain entities such as large financial institutions, insurers, and listed companies to report climate-related information such as governance structures and risk management frameworks for addressing and managing climate-related risks, climate-related strategy impacts, and greenhouse gas emission data.

The New Zealand climate standards were developed in tandem with the ISSB IFRS S1 and S2 standards to ensure compatibility. However, the New Zealand standards include a strong emphasis on incentivizing partnerships with indigenous Māori tribes and feature phased-in adoption compliance to ease the reporting burden on smaller firms. New Zealand’s Climate-Related Disclosures Regime focuses on the financial sector whereas CA SB 219 and other jurisdictions adoptions of ISSB IFRS S1 and S2 standards applies to a broader range of companies and industries.

Australia

The Australian Sustainability Reporting Standards (ASRS) have adapted IFRS S1 to make their voluntary ASRS 1 standard for general sustainability-related disclosures and IFRS S2 to their mandatory ASRS 2 standard for their climate-related financial disclosures. Alongside making one standard voluntary and the other mandatory, there are a few key differences between the IFRS S1 and S2 standards and the ASRS 1 and 2 standards.

Conclusion

The global sustainability reporting landscape is changing daily as regulators balance the need to protect the climate and inform the public, while ensuring that businesses remain competitive globally. While the current state of reporting may seem fragmented, there is an increasing effort across the world to unify requirements to make them more comparable across countries and reduce the number of burdens that companies face when complying.

At GSI, we are monitoring these changes closely to ensure that our clients are well prepared for the future of sustainability reporting. If your organization has questions about what regulations might apply to you or how your current reporting meets these standards, please reach out to us and we would be happy to discuss.

Over two days in June, sustainability leaders from across Europe and beyond gathered at Reuters’ Sustainability Reporting Europe conference to discuss CSRD...

Over two days in June, sustainability leaders from across Europe and beyond gathered at Reuters’ Sustainability Reporting Europe conference to discuss CSRD and sustainability reporting, debate the future of non-financial disclosure, explore the role of technology in reporting, and chart a path toward more integrated, impactful sustainability practices. Senior Sustainability Analyst Jannika Ilievska Kremer from GSI Environmental was in attendance, and the following are her key takeaways—covering overarching themes, why they matter for companies globally, and their relevance for U.S. firms.

1. Interoperability and Strategic Alignment

Speakers from GRI, IFRS/ISSB, and TNFD stressed that true interoperability must be built on shared principles and closely tied to corporate strategy.

Why this matters to companies: Without interoperability, firms end up juggling multiple, disjointed reporting systems—wasting resources and confusing stakeholders. By aligning frameworks and embedding disclosures into corporate strategy, organizations can streamline data collection, improve decision-making, and strengthen investor confidence.

Why it’s important for U.S. companies: U.S. firms operating globally face a patchwork of disclosure requirements; interoperability reduces complexity and helps ensure consistent, credible reporting across jurisdictions.

2. From Voluntary to Mandatory: Navigating Regulated Reporting

Member of European Parliament Lara Wolters warned that “simplification” proposals for CSRD/CSDDD may undermine accountability, and urged companies to stay the course—investing in ESG capabilities for strategic decision-making rather than treating compliance as a checkbox.

Why this matters to companies: As sustainability reporting shifts from voluntary best practices to mandatory regulations, early investment in robust systems turns a compliance burden into a competitive advantage by embedding ESG into core operations.

Why it’s important for U.S. companies: With state regulators moving toward their own disclosure mandates, U.S. companies will similarly benefit from proactive preparation and systems that handle both voluntary and compulsory reporting. Using GRI voluntary standards and former TCFD now IFRS S2 will prepare companies well.

3. Embedding Sustainability in Finance and Audit

Post-CSRD, finance and audit teams have moved to the center of sustainability reporting:

Why this matters to companies: Integrating ESG into finance ensures that sustainability data meets the same rigor as financial figures—boosting credibility with investors and enabling better risk management across the business.

Why it’s important for U.S. companies: U.S. investors and lenders increasingly demand ESG metrics alongside financial statements; having finance-vetted ESG data improves access to capital and reduces audit surprises. Completing a double materiality assessment or climate and opportunities assessment to understand your impact on the world, and the world’s impact on your company, is a good starting point for meeting stakeholder expectations.

4. Coordinating Cross-Functional Reporting

Corporate practitioners (Suntory, INGKA Group, Ahold Delhaize, Textile Exchange) shared that they:

Why this matters to companies: Siloed ESG efforts often fail. Cross-functional coordination ensures that sustainability insights inform strategy, operations, and communications—delivering real business value.

Why it’s important for U.S. companies: American firms with diverse operations need integrated dashboards and governance structures to satisfy both domestic and global stakeholder expectations. Completing a gap assessment of your ESG and Climate Governance, Strategy, Metrics and Targets, and Risk Management policies and processes is a good place to start.

5. Championing Double Materiality Assessments

Leaders from Henkel, ofi, and UCB underscored that DMA is an intensive process but yields strategic value when integrated thoughtfully across risk, governance, and business planning. Early engagement, cross-functional coordination, and clear documentation are essential to success. These waves 1 reporting entities also emphasized that DMAs

Requires targeted stakeholder interviews over generic surveys.

Demands early auditor involvement and rigorous documentation.

Should be revisited when regulations or business contexts change.

Why this matters to companies: Double materiality links sustainability risks and impacts directly to financial performance and strategy—enabling firms to allocate resources where they matter most and disclose information investors and society care about.

Why it’s important for U.S. companies: As U.S. state regulators move toward “financial materiality” disclosures (see CA Senate Bill 261 or NY Senate Bill 3697), a robust DMA framework helps companies demonstrate both risk management and societal impact, meeting varied stakeholder demands including regulatory compliance needs.

6. Europe’s Omnibus at the Crossroads

During a townhall session, representatives from Halton, Toyota, and CSR Europe examined the EU’s Omnibus recalibration, noting that many companies had overestimated their readiness for the original CSRD rapid regulatory rollout. Panelists called for a more streamlined approach that aligns with existing standards, encourages stakeholder engagement, and rewards early adopters. They emphasized that regulatory clarity and transparency are essential to prevent new requirements from undermining corporate competitiveness. Rather than pausing their efforts, these companies are leveraging the additional time afforded by the Omnibus delay to enhance staff training, close existing gaps, and embed sustainability more deeply into their innovation processes and customer engagement strategies.

Why this matters to companies: Clear, stable regulations enable companies to plan long-term investments in sustainability without facing unexpected compliance hurdles or costs. The Omnibus delay will afford companies more time to prepare.

Why it’s important for U.S. companies: U.S. multinationals need to navigate both EU Omnibus rules and emerging U.S. frameworks—stability in one region can make global compliance more manageable.

7. Harnessing Technology and AI

Microsoft and Cisco executives emphasized that technology must serve to enhance genuine sustainability efforts rather than substitute for them. While AI holds the potential to streamline research, modeling, and reporting, its effective adoption depends on meaningful behavioral change and strong digital literacy. When asked what the companies are doing to be more efficient in their data energy use the company representatives explained that at Microsoft, innovation is focused on data center efficiency—introducing closed-loop cooling systems and developing PFAS-free cooling fluids through AI—while Cisco has committed to circular design, ensuring that 100% of its new products are built with resource recovery and minimal waste in mind.

Why this matters to companies: Effective tech adoption reduces resource intensity, automates data workflows, and frees teams to focus on strategy—maximizing ROI on sustainability investments.

Why it’s important for U.S. companies: With U.S. firms facing rising energy costs and ESG scrutiny on a state and global and by local stakeholders, AI-driven efficiency and circular design offer both cost savings and stronger sustainability credentials.

8. Learning from Finance

The draft Omnibus proposal does not alter the initial requirement for limited assurance on CSRD reports (covering FY 2024 data published in 2025) but removes the Commission’s mandate to introduce a transition to reasonable assurance by October 1, 2028, effectively freezing the assurance standard at the limited level going forward. Whether limited or reasonable assurance, finance teams have decades of experience maintaining complete audit trails, version controls, and reconciliations for transactions. By mirroring these practices in ESG data collection—documenting methodologies, source data, and adjustments—ESG teams can dramatically reduce the time and cost of external assurance while increasing confidence in reported metrics. Nokia, Group Head of Sustainability Strategy and Disclosures and Standard Chartered, and EBRD (European Bank of Reconstruction Development) shared best practices for audit-ready ESG systems:

Establish strong internal controls and detailed documentation.

Engage assurance providers early to align on methodologies.

Drive digitization and cross-departmental alignment to scale reliable disclosures.

Why this matters to companies: Companies in scope of CSRD should use this time to build readiness. Audit readiness not only ensures compliance, but also builds trust with investors, regulators, and customers—an essential foundation for long-term sustainability.

Why it’s important for U.S. companies: U.S. companies are already navigating mandated assurance under California’s SB 253, which requires limited third-party verification of Scope 1 and 2 GHG emissions, with discussions underway to extend similar requirements to climate-risk disclosures under SB 261. Beyond statute, issuers of green and sustainability-linked bonds routinely secure independent verification to certify use-of-proceeds and performance targets, while major investors and ESG rating agencies increasingly view external assurance as a critical “quality signal.” Looking ahead, similar verification provisions are likely to emerge in other states (such as New York) and international frameworks—prompting U.S. firms to build rigorous controls and auditor partnerships now to stay ahead of evolving assurance expectations.

Conclusion

The Reuters Sustainability Reporting Europe conference underscored that the next phase of sustainability disclosure hinges on interoperability, strategic integration, cross-functional collaboration, and prudent use of technology. For U.S. companies—simultaneously managing domestic requirements and global frameworks—these takeaways offer a roadmap to transform compliance into competitive advantage.

We are approaching the midpoint of 2025, and the global landscape is becoming more uncertain and unstable—geopolitical, environmental, societal, economic, and technological...

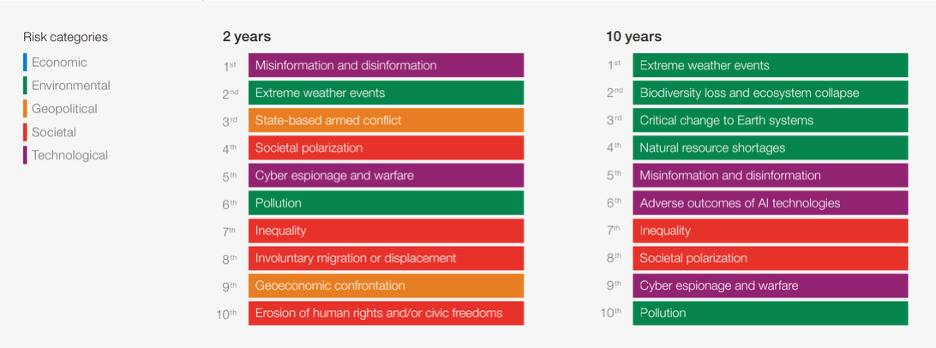

We are approaching the midpoint of 2025, and the global landscape is becoming more uncertain and unstable—geopolitical, environmental, societal, economic, and technological risks are becoming more complex and urgent. Climate-related financial risk management is highlighted in the World Economic Forum’s 2024-2025 Global Risk Perception Survey, which gathers insights from over 900 experts around the world. The report analyses global risks through three timeframes to support decision makers in balancing current crises and longer-term priorities. Environmental risks associated with extreme weather events are considered to have the second-highest material impact—trailing only armed conflict at the present time horizon, and misinformation over the next two years. These environmental impacts are expected to intensify over the next decade (see Fig. 1).

Figure 1. Global risks ranked by severity over the short and long term. Source: World Economic Forum Global Risks Perception Survey 2024-2025.

Extreme weather events already have huge impacts on local, national and global economies. Hurricane Helene, which struck the southeastern United States in late September 2024, had a profound impact on both regional and national economies. It is estimated that the total U.S. economic losses from the hurricane are between $225 billion and $250 billion. While the national GDP impact was relatively modest, the hurricane’s effects were significant in specific sectors and regions. For example, supply chain disruptions led to temporary halts in vehicle production at major facilities, affecting employment and output in those areas. The hurricane’s effects on infrastructure, businesses and reginal economies highlight the need for enhanced resilience and preparedness strategies.

It’s no surprise that investors and regulators worldwide have come to agree on the importance of climate-related financial risk reporting (Fig. 2). The California Senate Bills 253 and 261, amended to 219, reflect this global momentum. CA SB 261 references the TCFD recommendations, which for clarification were disbanded in 2023 and fully incorporated into the International Sustainability Standards Board (ISSB) IFRS S1 – General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 – Climate-related Disclosures (thus standardizing what was previously guidance in TCFD). Both IFRS S2 and TCFD require companies to disclose the processes and policies used to identify, assess, and manage climate-related risks (we will be sharing a detailed comparison between TCFD, IFRS S2 and other international mandates in the coming weeks). Investors want companies to disclose under TCFD/IFRS S2 to help them make informed, long-term investment decisions. While many jurisdictions have adopted IFRS S2, some like CA SB 261, reference TCFD as a foundation for climate reporting, either due to ongoing transitions or continued recognition of TCFD’s importance.

Figure 2. Global momentum of climate-related disclosures. According to the most recent IFRS Report, over 30 jurisdictions represent 57% of global GDP, more than 40% of global market capitalization, and more than half of global greenhouse gas emissions, have already finalized decisions on the adoption or other use of ISSB Standards, or are making progress to adopt or otherwise use the standards.

At GSI, we work with companies across various industries that may not have previously considered how to integrate climate-related risks—like physical risks (e.g., extreme weather) and transition risks (e.g., carbon regulations)—into their broader risk management processes. Fortunately, many companies already have established risk management processes in place, making it easier to integrate climate-related risks into these systems rather than developing a completely new process.

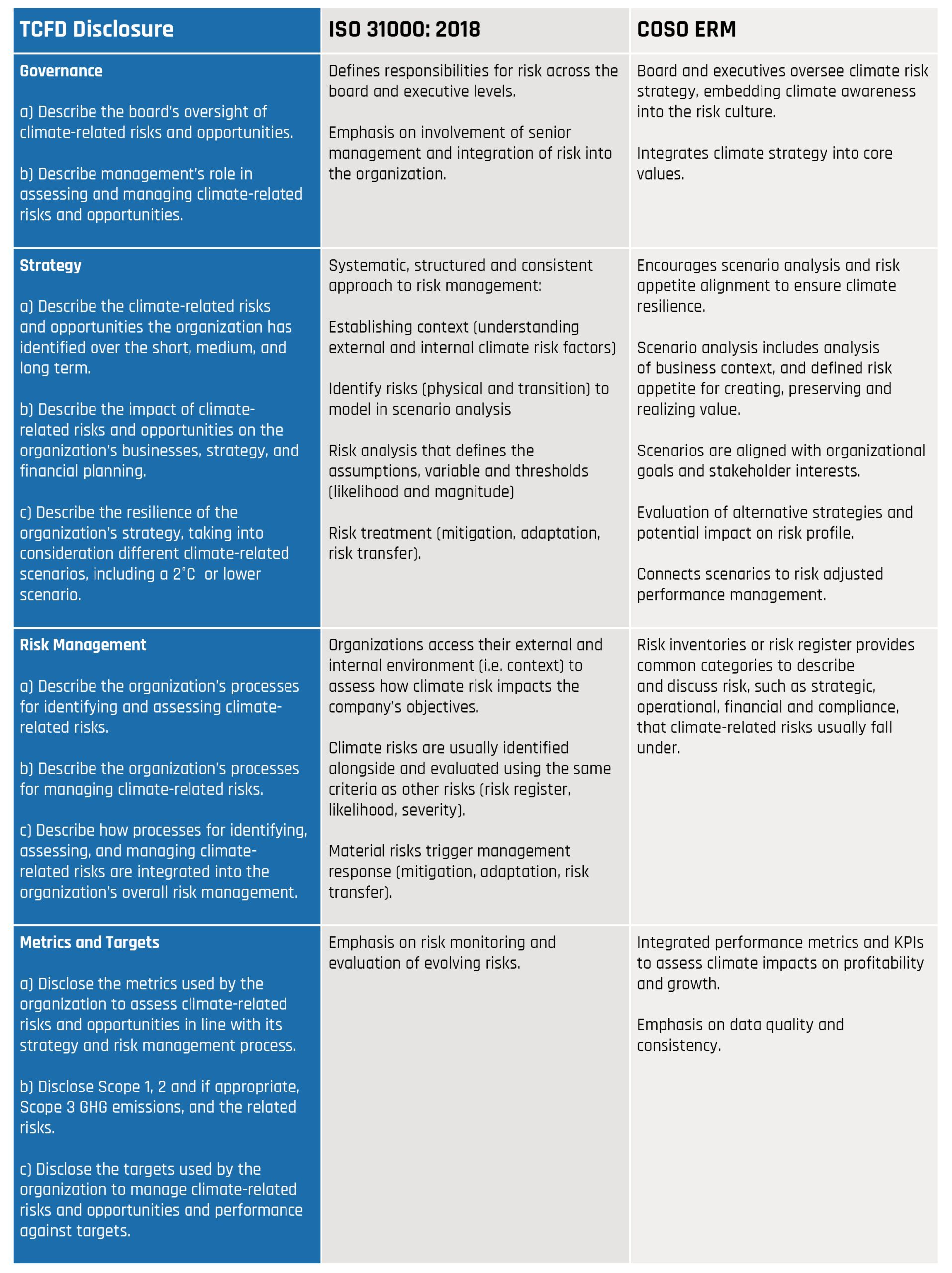

Whether a company already has a risk management system in place or is considering implementing one, ISO 31000, the international standard for risk management, and COSO ERM (Enterprise Risk Management) offer well-established, recognizable, and credible processes to build upon. ISO 31000 provides a structured and adaptable methodology for identifying, assessing, and treating risks, including those related to climate change. The COSO ERM Framework provides a strategic and integrated approach to risk management that is well-suited to support climate risk assessment. While not climate-specific, COSO’s emphasis on governance, strategy alignment, and performance makes it a powerful tool for embedding climate risk into broader enterprise planning—especially when conducting scenario analysis. By integrating climate risk and scenario planning with a standardized risk management system, companies can align these processes with their existing strategic planning cycles, helping to inform corporate, business, and functional strategies. To make the case for integration, GSI, we have summarized the synergy between the TCFD Disclosure, ISO 31000, and COSO ERM in Table 1 below.

Table 1. Synergies between existing risk management principles We increasingly see and encourage clients to consider implementing or reference existing ISO 31000 or COSO ERM in their climate disclosures. For example, a multinational company might say something like “Our enterprise risk management approach follows ISO 31000 principles, and climate-related risks are integrated into this framework through structured risk identification, evaluation and treatment processes” or “Our risk governance aligns with the COSO ERM to ensure climate risks are integrated into the company’s strategic outlook.” They may highlight how climate risk is embedded into their risk register, or the roles of risk owners and governance committees.

We increasingly see and encourage clients to consider implementing or reference existing ISO 31000 or COSO ERM in their climate disclosures. For example, a multinational company might say something like “Our enterprise risk management approach follows ISO 31000 principles, and climate-related risks are integrated into this framework through structured risk identification, evaluation and treatment processes” or “Our risk governance aligns with the COSO ERM to ensure climate risks are integrated into the company’s strategic outlook.” They may highlight how climate risk is embedded into their risk register, or the roles of risk owners and governance committees.

As global risks continue to intensify, integrating climate-related risks into existing risk management systems is more crucial than ever. By aligning climate risk with established frameworks like ISO 31000 and COSO ERM, companies can take meaningful steps to incorporate climate considerations into their broader strategic planning, ensuring resilience and long-term success. If companies are not able to implement ISO or COSO, we are still able to use the frameworks and concepts to make our client’s risk management processes more robust. Ultimately, disclosing climate-related risks helps companies build credibility, demonstrating that their processes are well-structured, globally recognized, and aligned with best practices in sustainability and governance, all while enhancing their ability to manage the most significant risks facing their business today and in the future.

If this information is useful to you or you have questions about climate-related financial risk management or how to start integrating climate into your existing processes, please feel free to reach out. Our team has decades of combined experience and is able to support all aspects of CA SB 219 compliance.